TL;DR

As an FCA-authorised expert with over 900,000 policies of various kinds arranged for our clients, WeCovr has a unique view of the UK consumer landscape. We're seeing unprecedented interest in private medical insurance, driven largely by growing concerns over NHS waiting times for crucial diagnostic tests and treatments.

Key takeaways

- Anxiety and Stress: The uncertainty of not knowing what is wrong can be debilitating, affecting mental health, sleep, and relationships.

- Worsening Conditions: For some illnesses, a delay in diagnosis can lead to the condition progressing, potentially making it harder to treat and leading to poorer long-term outcomes.

- Impact on Work and Life: Living with undiagnosed symptoms can make it difficult to work, care for family, or enjoy daily activities. This 'presenteeism' or outright absence from work also has a wider economic impact.

- An acute condition is a disease, illness, or injury that is likely to respond quickly to treatment and lead to a full recovery (e.g., a cataract, joint pain requiring replacement, a hernia).

- PMI does not cover pre-existing conditions. These are any health issues you had symptoms of, received advice for, or were treated for before your policy began.

As an FCA-authorised expert with over 900,000 policies of various kinds arranged for our clients, WeCovr has a unique view of the UK consumer landscape. We're seeing unprecedented interest in private medical insurance, driven largely by growing concerns over NHS waiting times for crucial diagnostic tests and treatments.

Market response to NHS testing delays

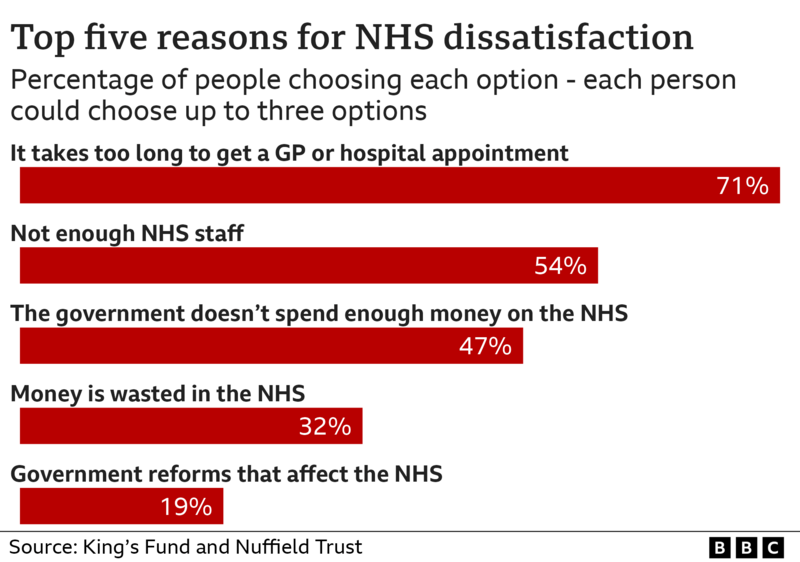

The relationship between the British public and the NHS is a cornerstone of our national identity. Yet, in recent years, this relationship has been strained by immense pressure on the system. The most visible symptom of this strain is the staggering length of waiting lists, particularly for diagnostic services. These aren't just numbers on a spreadsheet; they represent millions of individuals living with uncertainty, anxiety, and often, pain.

This national health challenge has triggered a significant shift in public behaviour. A growing number of people, from young professionals to families and retirees, are no longer willing to wait. They are proactively seeking alternatives to secure timely medical care, leading to a surge in demand for private medical insurance (PMI). The private healthcare market is responding directly to this need, offering a pathway to bypass the queues and gain rapid access to the tests and consultations that are so vital for peace of mind and effective treatment.

This article explores this trend in detail. We'll examine the reality of NHS diagnostic delays, explain how private health cover works as a practical solution, and provide the essential information you need to decide if it's the right choice for you and your family.

Understanding the NHS Diagnostic Waiting List Crisis

To grasp why so many are turning to private cover, it's essential to understand the scale of the challenge within the NHS. Diagnostic tests are the first critical step in identifying and understanding a health problem.

What are diagnostic tests? They are medical procedures used to confirm or rule out a condition. Common examples include:

- Imaging Scans: MRI, CT, and PET scans, which create detailed images of the inside of the body.

- Ultrasound: Uses sound waves to check on organs, tissues, and a developing baby during pregnancy.

- Endoscopy: A procedure where a thin tube with a camera is used to look inside the body, such as a colonoscopy or gastroscopy.

- Cardiology Tests: Such as an echocardiogram (ECG) to check heart function.

- Audiology Tests: To assess hearing loss.

The Sobering Statistics of 2025

As of early 2025, the figures from NHS England paint a stark picture. The overall waiting list for consultant-led elective care remains stubbornly high, affecting millions of people. Within this, the diagnostic waiting list is a major concern.

- Total Waiting List: The total number of people waiting for routine treatment continues to hover in the millions.

- Diagnostic Waits: A significant portion of these individuals, often well over 1.5 million, are specifically waiting for one of the 15 key diagnostic tests.

- The 6-Week Target: The NHS operational standard states that 99% of patients should wait no more than 6 weeks for a diagnostic test. In 2025, this target is being missed for a substantial percentage of patients, with hundreds of thousands waiting longer, some for many months.

(Source: Data trends extrapolated from official NHS England and Office for National Statistics reports, 2023-2024)

The Human Cost of Waiting

The impact of these delays extends far beyond inconvenience. For an individual, waiting for a diagnosis can be a period of immense psychological and physical distress.

- Anxiety and Stress: The uncertainty of not knowing what is wrong can be debilitating, affecting mental health, sleep, and relationships.

- Worsening Conditions: For some illnesses, a delay in diagnosis can lead to the condition progressing, potentially making it harder to treat and leading to poorer long-term outcomes.

- Impact on Work and Life: Living with undiagnosed symptoms can make it difficult to work, care for family, or enjoy daily activities. This 'presenteeism' or outright absence from work also has a wider economic impact.

Real-Life Example: Imagine Sarah, a 45-year-old teacher, who has been experiencing persistent knee pain. Her GP suspects a torn meniscus and refers her for an MRI scan on the NHS. She is told the waiting list is currently 14 weeks. For three and a half months, Sarah has to limit her mobility, struggle with pain during her active job, and live with the constant worry about the underlying cause. This is the reality for countless people across the UK.

How Private Medical Insurance Steps In as a Solution

Private Medical Insurance is designed to work alongside the NHS, providing a route to faster diagnosis and treatment for specific types of conditions. It acts as a safety net, giving you the option to 'go private' when you need it most.

The core promise of PMI is speed of access. Instead of joining a lengthy NHS queue, you can be seen by a specialist and undergo diagnostic tests within days or weeks.

The PMI Journey vs. The NHS Journey

Let's revisit Sarah's situation. If she had a private medical insurance policy, her journey would look very different.

| Step | NHS Journey | Private Medical Insurance Journey |

|---|---|---|

| 1. Initial GP Visit | Sarah sees her NHS GP who diagnoses the potential issue. | Sarah sees her NHS GP (or a private digital GP provided by her insurer). |

| 2. Referral | The GP refers her for an NHS MRI scan. | The GP provides an open referral for a private MRI scan. |

| 3. The Wait | Sarah is placed on the NHS waiting list. Wait time: 14 weeks. | Sarah calls her PMI provider to get the claim authorised. Time: 10-20 minutes. |

| 4. The Scan | After 14 weeks, Sarah gets her MRI scan at an NHS hospital. | The insurer provides a list of approved local private hospitals/clinics. Sarah books her scan. Appointment is within 1 week. |

| 5. Results & Follow-up | Sarah waits for the results and a follow-up NHS specialist appointment. Wait time: several more weeks. | The scan results are sent directly to her chosen private specialist. The consultation happens shortly after. |

| Total Time to Diagnosis | ~4-5 months | ~1-2 weeks |

This dramatic reduction in waiting time is the primary reason why UK consumers are increasingly investing in private health cover. It's about regaining control over your health journey and minimising the period of uncertainty.

Critical Information: What PMI Does and Does Not Cover

It is absolutely vital to understand the limitations of standard UK private medical insurance.

PMI is designed for acute conditions that arise after you take out the policy.

- An acute condition is a disease, illness, or injury that is likely to respond quickly to treatment and lead to a full recovery (e.g., a cataract, joint pain requiring replacement, a hernia).

- PMI does not cover pre-existing conditions. These are any health issues you had symptoms of, received advice for, or were treated for before your policy began.

- PMI does not cover chronic conditions. These are long-term illnesses that cannot be cured but can be managed, such as diabetes, asthma, or high blood pressure. These will always be managed by the NHS.

Understanding this distinction is key to having the right expectations for your policy.

The Surge in PMI Enquiries: A Look at the Numbers

The market data reflects the anecdotal evidence. There has been a clear and sustained increase in the number of people purchasing private medical insurance in the UK.

According to industry analysts like LaingBuisson and reports from the Association of British Insurers (ABI), the number of both individual and company-paid PMI policies has seen its most significant growth in over a decade.

- Changing Demographics: While traditionally seen as a perk for senior executives or the very wealthy, PMI is now being bought by a much wider audience. This includes self-employed individuals who cannot afford long periods off work, families wanting to protect their children's health, and younger people prioritising health security.

- The Broker's Role: With a more complex market and more first-time buyers, the role of an expert PMI broker has become more important than ever. A broker like WeCovr can help you navigate the dozens of policies available, comparing features and costs to find a plan that genuinely meets your needs and budget, at no extra cost to you.

What Does a Typical Private Health Insurance Policy Cover?

Not all PMI policies are the same. They are typically structured in tiers, allowing you to balance the level of cover with the premium you can afford.

Levels of Cover

- Basic (or In-patient only): This is the entry-level option. It covers the costs associated with being admitted to a hospital for treatment, including surgery, accommodation, and nursing care as an in-patient or day-patient. It often excludes initial diagnostics and consultations.

- Mid-Range (In-patient and Out-patient): This is the most popular level of cover. It includes everything in a basic policy, plus cover for outpatient services. This is crucial for diagnostics, as it covers specialist consultations and the scans (MRI, CT, etc.) needed to diagnose your condition before any hospital admission is required. This level often has financial limits on outpatient cover (e.g., £1,000 per year).

- Comprehensive: This top-tier cover provides extensive in-patient and outpatient cover, often with unlimited or very high financial limits. It may also include additional benefits like mental health support, dental and optical cover, and alternative therapies.

| Feature | Basic Cover | Mid-Range Cover | Comprehensive Cover |

|---|---|---|---|

| In-patient & Day-patient Care | ✅ Yes | ✅ Yes | ✅ Yes |

| Specialist Consultations (Outpatient) | ❌ No | ✅ Yes (Often with a limit) | ✅ Yes (Often unlimited) |

| Diagnostic Tests (Outpatient) | ❌ No | ✅ Yes (Often with a limit) | ✅ Yes (Often unlimited) |

| Mental Health Support | ❌ No | ➕ Optional Add-on | ✅ Often included |

| Therapies (e.g. physio) | ❌ No | ➕ Optional Add-on | ✅ Often included |

Understanding Key PMI Terms

- Underwriting: This is how an insurer assesses your medical history to decide what they will and won't cover.

- Moratorium Underwriting: This is the most common type. You don't declare your full medical history upfront. The insurer automatically excludes any condition you've had in the 5 years before the policy started. However, if you go 2 full years on the policy without any symptoms, treatment, or advice for that condition, it may become eligible for cover.

- Full Medical Underwriting (FMU): You provide your complete medical history when you apply. The insurer then tells you exactly what is excluded from day one. It takes longer but provides more certainty.

- Excess: This is a fixed amount you agree to pay towards any claim. For example, if you have a £250 excess and your treatment costs £3,000, you pay the first £250 and the insurer pays the remaining £2,750. A higher excess leads to a lower monthly premium.

- Hospital List: Insurers have lists of approved private hospitals. Your choice of list (e.g., local hospitals vs. a national list including prime London clinics) will affect your premium.

Choosing the Right PMI Provider: Key Factors to Consider

The UK has a mature and competitive private medical insurance market with several excellent providers. Each has its own strengths and focus.

| Provider | Key Differentiator / Focus Area | Best For... |

|---|---|---|

| Bupa | One of the largest and most well-known providers with an extensive network of its own clinics and facilities. | Those seeking a trusted brand with a comprehensive network. |

| AXA Health | Strong focus on clinical expertise and customer support, offering a range of flexible plans. | Individuals and businesses looking for high-quality, reliable cover. |

| Aviva | A major UK insurer offering a 'back to health' promise and a clear, straightforward approach to claims. | Customers who value the security of a large, established financial institution. |

| Vitality | Unique wellness-based model that rewards members for healthy living with discounts and benefits. | Active individuals who want to be rewarded for staying healthy. |

| WPA | A not-for-profit organisation often praised for its excellent customer service and flexible policies. | Those who prioritise customer service and a more personal approach. |

This is just a snapshot. Comparing these providers on a like-for-like basis can be complex due to differences in their policy wording, benefit limits, and hospital lists. This is where an independent broker like WeCovr provides invaluable assistance, offering impartial advice across the market to find the best PMI provider for your specific circumstances.

The Cost of Peace of Mind: Understanding PMI Premiums

The cost of private medical insurance is highly personal and depends on a range of factors. There is no 'one-size-fits-all' price.

Your monthly premium will be calculated based on:

| Factor | How it Affects Your Premium |

|---|---|

| Age | Premiums increase with age, as the statistical likelihood of needing to claim grows. |

| Location | Living in areas with higher private medical costs (like London) will result in a higher premium. |

| Level of Cover | Comprehensive plans cost more than basic in-patient only plans. |

| Excess | Choosing a higher excess (e.g., £500 instead of £100) will significantly lower your premium. |

| Underwriting | The type of underwriting chosen can sometimes influence the initial price. |

| Hospital List | A plan with access to premium central London hospitals will be more expensive than one with a local network. |

| Lifestyle | Smokers will pay a higher premium than non-smokers. |

As a rough guide, a healthy 30-year-old might find a mid-range policy starting from £40-£50 per month, while a 50-year-old could expect to pay £80-£120 or more for similar cover. These are purely illustrative, and your actual quote will be unique to you.

Beyond Diagnostics: The Added Value of Modern PMI Policies

Today's private health cover offers much more than just fast-track surgery. Insurers are increasingly focused on keeping their members healthy and providing holistic support.

- Digital GP Services: Most major policies now include access to a virtual GP, often 24/7. You can get a video consultation from your home or office, receive advice, and get prescriptions without waiting for an NHS GP appointment.

- Mental Health Support: Recognising the growing mental health crisis, many insurers now include cover for a set number of counselling or therapy sessions as standard, providing rapid access to support for issues like anxiety, stress, and depression.

- Wellness Programmes: Providers like Vitality have pioneered the concept of rewarding healthy behaviour. By tracking your activity, you can earn points that translate into real-world benefits like free cinema tickets, coffee, and discounts on gym memberships or smartwatches.

- Exclusive Member Benefits: When you arrange a policy through an expert like WeCovr, you can receive additional perks. We provide our health and life insurance clients with complimentary access to our AI-powered calorie and nutrition tracking app, CalorieHero, to support their wellness goals. Furthermore, clients often receive discounts on other insurance products, such as life or income protection insurance, creating a more comprehensive financial safety net.

Navigating the Claims Process: A Step-by-Step Guide

Making a claim on your PMI is designed to be a simple, stress-free process.

- See Your GP: Your journey almost always starts with your NHS GP. You discuss your symptoms, and they recommend you see a specialist. Ask for an open referral, which means they refer you to a type of specialist (e.g., a dermatologist) rather than a named individual.

- Contact Your Insurer: Call your PMI provider's claims line. You'll need your policy number and the details of your GP's referral. They will check your cover and authorise the claim, giving you a pre-authorisation number.

- Book Your Appointment: Your insurer will provide a list of approved specialists and private hospitals in your area. You then call the hospital or specialist's secretary directly to book your consultation or diagnostic scan, quoting your pre-authorisation number.

- Attend and Get Treated: You attend your private appointment. You do not need to pay anything (unless you have an excess, which is usually handled at the end of the treatment episode).

- Direct Settlement: The hospital or clinic sends the invoice directly to your insurance company, who settles the bill on your behalf.

The process is designed to remove the financial and administrative burden from you, allowing you to focus purely on your health.

Does private health insurance cover pre-existing conditions?

Can I still use the NHS if I have private medical insurance?

What's the difference between moratorium and full medical underwriting?

Is it cheaper to go through a broker like WeCovr?

Take Control of Your Health Today

The peace of mind that comes from knowing you can access fast, high-quality medical diagnostics and treatment is invaluable. In a time of record NHS waiting lists, private medical insurance offers a practical and increasingly popular solution.

Navigating the market can be complex, but you don't have to do it alone.

Contact WeCovr today for a free, no-obligation quote. Our friendly, expert advisors will help you compare the UK's leading insurers and find the perfect private health cover for your needs and budget.

Sources

- NHS England: Waiting times and referral-to-treatment statistics.

- Office for National Statistics (ONS): Health, mortality, and workforce data.

- NICE: Clinical guidance and technology appraisals.

- Care Quality Commission (CQC): Provider quality and inspection reports.

- UK Health Security Agency (UKHSA): Public health surveillance reports.

- Association of British Insurers (ABI): Health and protection market publications.