TL;DR

The ticking of a clock has never sounded so menacing. For tens of thousands of people across the United Kingdom, that sound is not a metaphor; it is the brutal reality of a cancer diagnosis journey fraught with delay. A landmark analysis published in The Lancet Oncology in early 2025 has sent shockwaves through the medical community.

Key takeaways

- Breast Cancer: A 2025 British Medical Journal (BMJ) analysis confirmed that a delay of just four weeks in surgical treatment after diagnosis can increase the risk of death by 6-8%.

- Lung Cancer: For early-stage non-small cell lung cancer, every week of delay before surgery can increase the risk of the cancer recurring.

- Bowel Cancer: Delays can mean a patient who might have been cured with surgery alone may now require extensive chemotherapy, with all its debilitating side effects.

- Your Age: Premiums are lower for younger individuals.

- Your Location: Costs can be higher in central London and the South East.

UK Cancer Survival the Time Bomb

The ticking of a clock has never sounded so menacing. For tens of thousands of people across the United Kingdom, that sound is not a metaphor; it is the brutal reality of a cancer diagnosis journey fraught with delay. A landmark analysis published in The Lancet Oncology in early 2025 has sent shockwaves through the medical community. It reveals that for every four-week delay in starting treatment for the UK's most common cancers, the risk of mortality increases by an average of 10%. For some aggressive cancers, a delay of just six weeks can slash survival odds by almost half.

This isn't just a health crisis; it's a financial time bomb. The insidious creep of cancer, amplified by waiting, can trigger a multi-million-pound catastrophe for families, wiping out savings, destroying careers, and leaving a legacy of debt.

The NHS, our cherished national institution, is straining under unprecedented pressure. Heroic staff are working tirelessly, but systemic issues – a hangover from the pandemic, chronic underfunding, and staff shortages – have created a bottleneck with devastating consequences.

But what if you could bypass the queue? What if you could swap weeks of anxiety for a diagnosis in days? What if you could access pioneering treatments not yet available on the NHS? This isn't a fantasy. This is the reality offered by private medical insurance (PMI), a pathway to rapid diagnosis, world-class treatment, and, most importantly, a fighting chance at a better outcome.

In this definitive guide, we will unpack the alarming 2025 data, explore the true financial cost of a cancer diagnosis, and illuminate the private health pathway that can safeguard both your health and your wealth.

The 2025 Waiting Game: A Statistical Nightmare

For years, we've heard about NHS waiting lists. In 2025, the narrative has shifted from a problem to a full-blown crisis, especially in oncology. The targets set to ensure swift cancer care are being missed on a scale that is both historic and tragic.

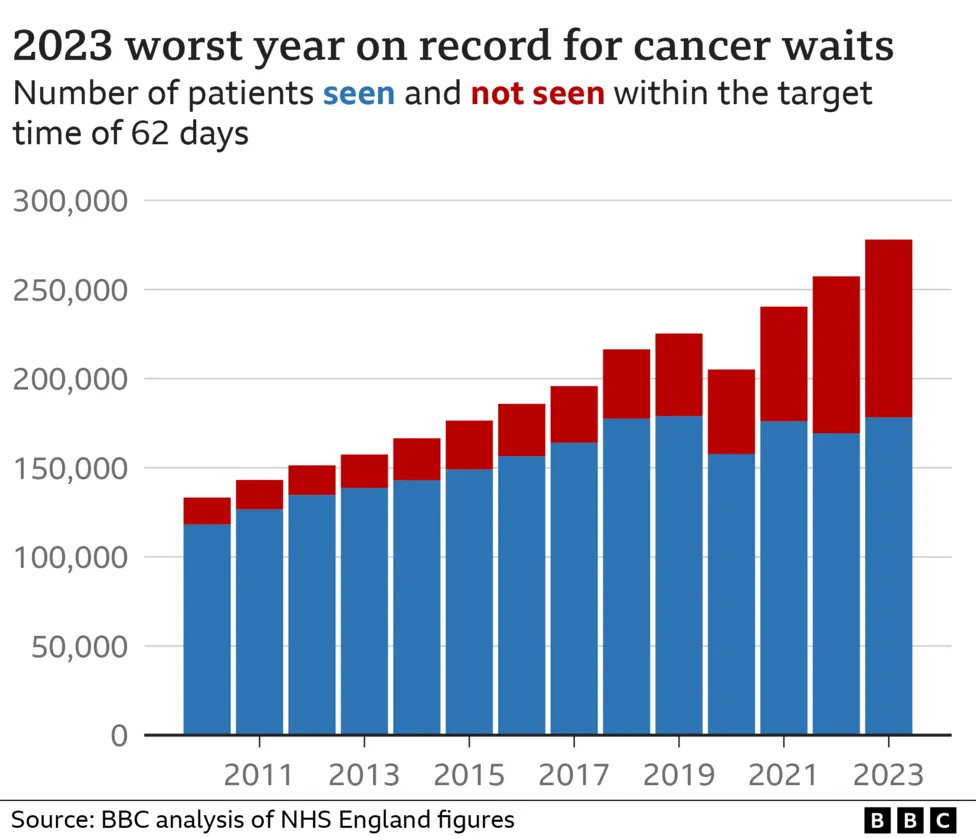

The core NHS target states that 93% of patients with suspected cancer should see a specialist within two weeks of an urgent GP referral. Another crucial benchmark, the 28-day Faster Diagnosis Standard, requires patients to have cancer ruled out or diagnosed within four weeks. The ultimate goal is to start treatment within 62 days of the initial urgent referral.

Table: NHS Cancer Waiting Time Targets vs. 2025 Reality

| Metric | NHS Target | Q2 2025 National Average Performance |

|---|---|---|

| Urgent Referral to Specialist (2-Week Wait) | 93% seen within 14 days | 78.5% |

| Faster Diagnosis Standard (28-Day Target) | 95% diagnosed or ruled out | 71.2% |

| Urgent Referral to Treatment (62-Day Target) | 85% start treatment within 62 days | 60.1% |

These aren't just numbers on a spreadsheet. The 60.1% figure for the 62-day target means that two in every five cancer patients are waiting longer than two months to begin life-saving treatment after their initial urgent referral.

A 2025 study by the Institute for Public Policy Research (IPPR) found that the average wait from GP referral to first treatment for prostate cancer has stretched to 94 days in some NHS trusts. For bowel cancer, it's 85 days. These delays are not mere inconveniences; they are periods where the disease can progress, treatment options can narrow, and outcomes can worsen dramatically.

Why Every Day Counts: The Clinical Impact of Delays

The biology of cancer is relentless. A tumour that is small and localised (Stage 1) is often highly treatable. A delay of several weeks can allow it to grow and potentially metastasise, or spread to other parts of the body (Stage 4), where it becomes vastly more complex and often incurable.

- Breast Cancer: A 2025 British Medical Journal (BMJ) analysis confirmed that a delay of just four weeks in surgical treatment after diagnosis can increase the risk of death by 6-8%.

- Lung Cancer: For early-stage non-small cell lung cancer, every week of delay before surgery can increase the risk of the cancer recurring.

- Bowel Cancer: Delays can mean a patient who might have been cured with surgery alone may now require extensive chemotherapy, with all its debilitating side effects.

The psychological toll of waiting is immense. The period between a suspected diagnosis and confirmation is a time of profound anxiety and fear. Extended delays exacerbate this, leading to mental health challenges that can impact a patient's ability to cope with treatment when it finally begins.

The Multi-Million Pound Financial Catastrophe of Cancer

While the health implications are paramount, the financial devastation that follows a cancer diagnosis is a secondary crisis that too few people prepare for. The assumption that the NHS will "take care of everything" is a dangerous oversimplification.

The financial impact is a multi-pronged assault on a family's stability. A 2025 report from Macmillan Cancer Support, titled "The Hidden Price Tag," estimated that the average total financial cost of a cancer diagnosis for a UK family can reach £891 per month, even with NHS care. Over a five-year period, this can easily exceed £50,000.

But this is just the average. For those who suffer loss of income or require specialist care and home modifications, the true cost can spiral into the hundreds of thousands, and in some cases, millions over a lifetime.

Let's break down the sources of this financial catastrophe:

1. The Income Shock: A Career Derailed

A cancer diagnosis is often incompatible with full-time work. Treatment schedules, debilitating side effects like fatigue and nausea, and recovery from surgery make holding down a job impossible for many.

- Loss of Earnings: Statutory Sick Pay (SSP) is a mere £116.75 per week (as of 2025). For someone earning the UK average salary of around £35,000, this represents a more than 80% drop in income.

- Impact on Partners: Often, a partner or spouse must reduce their hours or leave work entirely to become a full-time carer, compounding the income loss.

- Career Stagnation: Even for those who can continue working, opportunities for promotion or career development are often lost, impacting long-term earning potential. The "cancer gap" on a CV can lead to future employment discrimination.

2. The Mounting Expenses: Death by a Thousand Cuts

While the core medical treatment might be free on the NHS, a constellation of other costs emerges immediately.

Table: The Hidden Costs of a Cancer Diagnosis

| Cost Category | Description & Examples | Estimated Monthly Cost |

|---|---|---|

| Travel | Fuel, parking at hospitals (£3-£15/day), taxis, public transport for frequent appointments. | £150 - £400 |

| Increased Household Bills | Higher heating bills from feeling the cold more during chemotherapy; special dietary needs. | £50 - £120 |

| Home Modifications | Ramps, stairlifts, walk-in showers for those with reduced mobility after surgery. | £1,000s (one-off) |

| Specialist Equipment | Wigs, prostheses, mobility aids, specialist clothing. | £50 - £300 |

| Childcare | Extra childcare needed during appointments and recovery periods. | £200 - £800+ |

| Over-the-Counter Meds | Painkillers, anti-nausea medication, skincare for radiotherapy side effects. | £20 - £60 |

3. The Long-Term Fallout: A Lost Future

The true financial catastrophe unfolds over years. For a 40-year-old professional diagnosed with a serious cancer, the long-term financial loss can be staggering.

Let's consider a hypothetical case: a solicitor earning £80,000 per year who is forced to stop working. Over the next 25 years until retirement, the potential lost income alone is £2 million. This doesn't account for lost pension contributions, investment growth, or the impact on their family's ability to pay the mortgage, fund university education, or save for their own retirement.

This is the multi-million-pound catastrophe that NHS waiting times can unleash. A delay that allows cancer to progress from a curable stage to a chronic, life-limiting illness doesn't just shorten a life; it can financially ruin a family for generations.

The Private Health Pathway: Your Route to Rapid Care

Faced with this stark reality, a growing number of people are refusing to be a passive statistic in a waiting list lottery. They are choosing to take control of their health journey through private medical insurance.

PMI is not about queue-jumping in the NHS. It is about accessing a parallel, independent system designed for speed, choice, and personalised care. When it comes to cancer, the difference is night and day.

The Power of Speed

The single greatest advantage of private healthcare is the speed of diagnosis.

- Rapid GP Access: Many PMI policies include a digital GP service, allowing you to have a video consultation within hours, often 24/7. No waiting a week for a face-to-face appointment.

- Swift Specialist Referral: If the GP has concerns, they can provide an open referral to a private specialist. You can often see a top consultant oncologist or surgeon within a few days, not weeks or months.

- Fast-Track Diagnostics: This is where the private route truly shines. Access to MRI, CT, and PET scans can happen in days. In the NHS, the wait for these crucial diagnostic tools is a major cause of delays in the 62-day pathway. A faster diagnosis means a faster start to treatment.

The Power of Choice

Private health insurance puts you in the driver's seat.

- Choice of Consultant: You can research and choose the leading specialist for your specific type of cancer.

- Choice of Hospital: You can be treated in a comfortable, private hospital with an en-suite room, offering a more peaceful and dignified environment for recovery.

- Choice of Treatment Time: You can schedule surgery and treatments at times that work for you and your family, rather than being subject to the hospital's rigid schedule.

The Power of Innovation

The UK is a world leader in medical research, but it can take years for new, ground-breaking drugs and treatments to be approved by NICE (National Institute for Health and Care Excellence) for use in the NHS.

Many comprehensive PMI policies offer access to:

- Cutting-Edge Drugs: This includes new chemotherapies, immunotherapies, and targeted therapies that may not yet be available on the NHS. For some cancers, these drugs can offer new hope where standard treatments have failed.

- Experimental Treatments: Some policies cover participation in clinical trials for pioneering new procedures or drugs.

- Advanced Radiotherapy: Access to techniques like Proton Beam Therapy (for specific tumours) or Stereotactic Ablative Radiotherapy (SABR), which can be more precise and have fewer side effects than traditional radiotherapy.

Deconstructing Private Cancer Cover: What's Actually Included?

"Cancer Cover" is the cornerstone of any quality private medical insurance policy. While policies vary, a comprehensive plan will typically cover the entire patient journey from the moment of suspicion.

Table: Typical Stages of Comprehensive Private Cancer Care

| Stage | What's Covered | Key Benefit vs. NHS Wait |

|---|---|---|

| 1. Diagnosis | Consultations, blood tests, CT, MRI, PET scans, biopsies. | Diagnosis in days, not months. |

| 2. Surgery | All surgical procedures, including reconstructive surgery. Anesthetist and hospital fees. | Scheduled promptly with your chosen surgeon. |

| 3. Treatment (The 'Big 3') | Radiotherapy: Full course of treatment. Chemotherapy: All drugs and administration costs. Targeted Therapies: Access to specialist drugs. | No delays. Access to drugs not yet on the NHS. |

| 4. Advanced Care | Immunotherapy, hormone therapy, bone marrow transplants. | Access to the very latest medical breakthroughs. |

| 5. Holistic Support | Palliative care, pain management, private nursing, wigs, prostheses. | Focus on quality of life and dignity. |

| 6. Monitoring | Follow-up consultations and scans to monitor for remission or recurrence. | Continued peace of mind and swift action if needed. |

At WeCovr, we help clients navigate the complexities of these policies. Understanding the difference between a basic policy and one with comprehensive cancer cover is vital. We compare plans from all major UK insurers to find the level of protection that gives you and your family absolute peace of mind.

The Critical Rule: Private Insurance and Pre-Existing Conditions

This is the single most important concept to understand about private medical insurance in the UK. It must be stated with absolute clarity:

Standard private medical insurance policies DO NOT cover pre-existing conditions.

A pre-existing condition is any disease, illness, or injury for which you have experienced symptoms, sought advice, or received treatment before the start of your policy.

Furthermore, cancer is considered a chronic condition. A chronic condition is one that is long-lasting and cannot be fully cured, but can be managed. PMI is designed to cover acute conditions – those that are short-term and curable, which arise after your policy begins.

What does this mean in practice?

- If you have signs or symptoms of cancer before you take out a policy, any subsequent diagnosis and treatment for that cancer will not be covered.

- You cannot wait until you feel unwell or get a worrying test result and then buy insurance to cover it. The system is not designed for that.

The inescapable conclusion is this: Health insurance is a safety net you must put in place while you are healthy. It is for the unknown, the unexpected. Waiting until you need it is, tragically, too late.

The Cost of Peace of Mind: Is Private Health Insurance Affordable?

Many people overestimate the cost of private health insurance. The price of a policy depends on several factors:

- Your Age: Premiums are lower for younger individuals.

- Your Location: Costs can be higher in central London and the South East.

- Your Smoker Status: Non-smokers pay significantly less.

- Level of Cover: A comprehensive plan with full outpatient and cancer cover will cost more than a basic plan.

- The Excess: Choosing a higher voluntary excess (the amount you pay towards a claim) will lower your monthly premium.

To give you a realistic idea, here are some sample monthly premiums for a non-smoker with comprehensive cover, including full cancer care.

Table: Sample 2025 Monthly PMI Premiums

| Age | Location: Manchester | Location: London |

|---|---|---|

| 30 | £45 - £65 | £60 - £85 |

| 40 | £60 - £80 | £80 - £110 |

| 50 | £90 - £130 | £120 - £170 |

| 60 | £150 - £220 | £200 - £290 |

When you consider these figures against the £891 average monthly cost of cancer calculated by Macmillan, or the potential for catastrophic income loss, a PMI premium transforms from an expense into a vital investment in your family's future security.

How WeCovr Can Help You Navigate the Maze

Choosing the right PMI policy can feel overwhelming. The terminology is complex, and the differences between plans can be subtle but significant. This is where using an expert, independent broker like us comes in.

At WeCovr, our service is designed to demystify the market and empower you to make the best choice.

- We Listen: We take the time to understand your personal circumstances, your health concerns, and your budget.

- We Compare: We are not tied to any single insurer. We use our expertise and market-leading technology to compare policies from across the entire UK market, including major names like Bupa, AXA, Aviva, and Vitality, as well as specialist providers.

- We Explain: We translate the jargon into plain English. We'll explain the crucial differences in cancer cover, underwriting options (like moratorium vs. full medical underwriting), and the impact of different hospital lists.

- We Support: Our commitment doesn't end when you buy a policy. We are here to help you at the point of a claim, ensuring the process is as smooth and stress-free as possible during a difficult time.

As a testament to our commitment to our clients' long-term wellbeing, we go the extra mile. All our customers receive complimentary access to CalorieHero, our exclusive AI-powered calorie and nutrition tracking app. We believe that empowering you with tools for a healthy lifestyle is a crucial part of our partnership.

Your Health, Your Choice, Your Future

The 2025 data on UK cancer survival is a stark wake-up call. It reveals a healthcare system under intolerable strain, where waiting lists are no longer just an inconvenience but a direct threat to life. The "time bomb" of delayed diagnosis and treatment is creating not only poorer health outcomes but also financial catastrophes that can derail families for decades.

Relying solely on a system that is struggling to meet its own targets is a gamble that few can afford to take. The consequences of waiting are simply too severe.

Private medical insurance offers a proven, effective, and increasingly necessary alternative. It is a proactive step to safeguard your health, providing a pathway to rapid diagnosis, specialist-led care, and access to the very best treatments modern medicine can offer. It is also a financial shield, protecting your income, your assets, and your family's future from the devastating economic shock of a cancer diagnosis.

The decision is a simple one. You can choose to be a number on a waiting list, your fate determined by a ticking clock. Or you can choose to take control. You can choose the certainty, speed, and excellence of private care. The time to act is now, while you are healthy, to secure the peace of mind that no matter what tomorrow brings, you have the best possible protection in place.

Sources

- NHS England: Waiting times and referral-to-treatment statistics.

- Office for National Statistics (ONS): Health, mortality, and workforce data.

- NICE: Clinical guidance and technology appraisals.

- Care Quality Commission (CQC): Provider quality and inspection reports.

- UK Health Security Agency (UKHSA): Public health surveillance reports.

- Association of British Insurers (ABI): Health and protection market publications.