TL;DR

The National Health Service (NHS) is one of Britain's most cherished institutions, a beacon of universal healthcare. Yet, the foundational pillar of the NHS – the General Practitioner (GP) service – is facing a crisis of unprecedented scale. New data for 2025 paints a stark and worrying picture: the wait for a routine GP appointment has spiralled, leaving millions of people in a painful limbo.

Key takeaways

- Your Budget: We help you understand the trade-offs between premium cost, your chosen excess (the amount you pay towards a claim), and the level of cover.

- Level of Cover: Do you just want core hospital cover, or is comprehensive out-patient cover for fast diagnosis your priority?

- Hospital List: Insurers offer different tiers of hospitals. A national list provides wide coverage, while a more limited local list can reduce your premium. Premium lists including prime central London hospitals cost more.

- Underwriting: We'll explain the pros and cons of Moratorium vs. Full Medical Underwriting for your specific circumstances.

- A staggering analysis of the latest NHS England appointment data reveals that in May 2025 alone, over 3.2 million appointments took place more than 28 days after they were booked.

UK Gp Wait Times Explode

The National Health Service (NHS) is one of Britain's most cherished institutions, a beacon of universal healthcare. Yet, the foundational pillar of the NHS – the General Practitioner (GP) service – is facing a crisis of unprecedented scale. New data for 2025 paints a stark and worrying picture: the wait for a routine GP appointment has spiralled, leaving millions of people in a painful limbo.

A staggering analysis of the latest NHS England appointment data reveals that in May 2025 alone, over 3.2 million appointments took place more than 28 days after they were booked. This isn't just an inconvenience; it's a public health emergency in slow motion. Behind these numbers are anxious parents, worried professionals, and vulnerable elderly individuals whose health concerns are left to fester. The delay risks turning treatable, acute conditions into chronic problems and, in the most tragic cases, allows serious diseases like cancer to progress undetected.

While the dedication of NHS staff remains unwavering, the system itself is buckling under immense pressure from funding gaps, a shortage of doctors, and a growing, ageing population with increasingly complex health needs.

For a growing number of Britons, the uncertainty and anxiety of this new reality are no longer acceptable. They are turning to a proactive solution that offers what the current system often cannot: speed, choice, and peace of mind. That solution is private health insurance.

This comprehensive guide will unpack the alarming reality of UK GP wait times, explore the profound human cost of these delays, and provide a definitive overview of how private medical insurance (PMI) offers an immediate and effective pathway to the primary care, specialist consultations, and diagnostic tests you need, when you need them most.

The Alarming Reality: Deconstructing the UK's GP Appointment Crisis

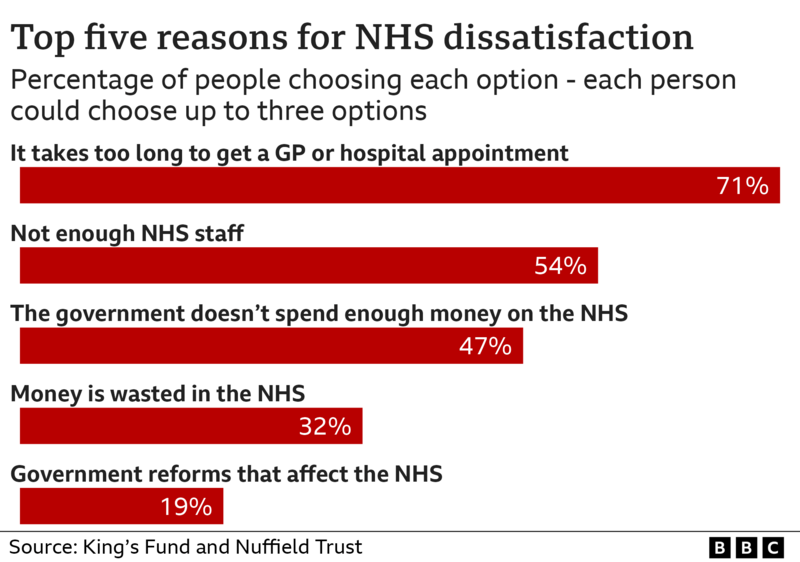

To understand the solution, we must first grasp the full scale of the problem. The GP appointment crisis is not a sudden event but the culmination of years of mounting pressures. The latest 2025 figures from NHS Digital and analysis from health think tanks like The King's Fund and the Nuffield Trust reveal a system stretched to its breaking point.

Let's look at the hard data:

- The 28-Day+ Wait: As highlighted, over 3.2 million appointments in May 2025 involved a wait of four weeks or more. This represents over 10% of all appointments, a significant increase from just 7% two years prior.

- The "8am Scramble": Millions describe the daily ritual of repeatedly calling their surgery at 8am, only to be met with engaged tones or a recorded message stating all appointments for the day have been taken.

- Shrinking GP Numbers: Data from the British Medical Association (BMA) shows that the number of fully qualified, full-time-equivalent GPs per 1,000 patients in England has fallen to a record low of 0.43 in early 2025, down from 0.52 a decade ago. We have fewer GPs serving a larger, sicker population.

- Intense Workload: The GPs who remain are dealing with an unsustainable workload. The average number of patients per GP in England has now surpassed 2,300, with many practices having lists far larger than this.

- Regional Disparities: The crisis is not felt equally. Patients in more deprived areas and certain regions like the South West and East of England are experiencing significantly longer waits than those in major urban centres like London, creating a postcode lottery for basic healthcare.

This data is not just a collection of numbers; it represents a fundamental breakdown in access to primary care. The table below, based on NHS England data for May 2025, illustrates the distribution of waiting times.

Table 1: UK GP Appointment Wait Times (NHS England - May 2025 Data)

| Wait Time | Number of Appointments (Approx.) | Percentage of Total |

|---|---|---|

| Same Day | 13.5 Million | 44% |

| 1-7 Days | 9.3 Million | 30% |

| 8-14 Days | 2.8 Million | 9% |

| 15-28 Days | 2.1 Million | 7% |

| Over 28 Days | 3.2 Million | 10.5% |

| Total | 30.9 Million | 100% |

Source: Analysis of NHS Digital 2025 appointment data.

While nearly half of appointments are delivered on the same day – a testament to the hard work of practice staff prioritising urgent cases – the significant and growing number of patients waiting over two, three, or even four weeks is the critical issue. These are often the "routine" appointments for persistent coughs, unusual moles, ongoing pain, or mental health concerns that, if left unchecked, can signal the start of something far more serious.

The Human Cost: Why Long GP Waits Are More Than Just an Inconvenience

A month-long wait for a GP is not a simple frustration. It has profound and dangerous consequences for individuals, the wider health service, and the economy.

1. Delayed and Missed Diagnoses

This is the most critical danger. The entire model of UK healthcare relies on the GP as a gatekeeper and diagnostician. When that gateway is blocked, the system fails.

- Cancer: Charities like Cancer Research UK have repeatedly warned that early diagnosis is the single most important factor in survival rates. A four-week delay in seeing a GP about a persistent symptom can be the difference between a treatable, early-stage cancer and an advanced, metastatic disease with a poor prognosis.

- Heart Conditions: Symptoms like breathlessness or chest pain need immediate evaluation. Delays can lead to undiagnosed heart disease, increasing the risk of a sudden, life-threatening event like a heart attack or stroke.

- Neurological Conditions: For conditions like Parkinson's or Multiple Sclerosis, early intervention can significantly slow disease progression and improve quality of life. Long waits rob patients of this crucial window.

Real-Life Scenario: Consider "David," a 52-year-old self-employed plumber. He noticed a change in bowel habits and intermittent abdominal pain. He tried for two weeks to get a routine appointment before finally securing one for a month's time. During the wait, his anxiety grew. By the time he saw the GP, his symptoms had worsened. The subsequent urgent referral confirmed bowel cancer, but it was at a more advanced stage than it might have been if he'd been seen and referred five or six weeks earlier.

2. Escalation of Acute Health Issues

Minor health problems, when ignored, rarely solve themselves. A simple urinary tract infection (UTI) can ascend to the kidneys and cause sepsis. A chest infection can develop into pneumonia. A painful joint, left without physiotherapy advice, can lead to chronic mobility issues. Timely GP intervention with antibiotics, referrals, or simple advice can prevent these costly and dangerous escalations.

3. The Toll on Mental Health

The process of trying and failing to get an appointment is incredibly stressful. The uncertainty of waiting with an undiagnosed health concern fuels anxiety and can exacerbate or even trigger mental health conditions. For those already suffering from depression or anxiety, the inability to access a trusted GP for support can be devastating, creating a vicious cycle of worsening physical and mental health.

4. Overburdening Emergency Services

Frustrated and worried, where do people turn when they can't see a GP? They go to A&E. A 2025 report from the Royal College of Emergency Medicine estimated that up to 30% of A&E attendees could have been more appropriately treated by a GP. This puts enormous strain on emergency departments, diverting resources from genuine life-threatening emergencies and contributing to the dangerously long A&E waiting times we now see across the country.

5. Economic Impact

The health of the nation is tied to the health of its economy. When people are waiting for appointments, they may be too unwell to work, leading to increased sick days. Others may attend work while ill ("presenteeism"), leading to drastically reduced productivity. The long-term economic cost of managing chronic conditions that could have been prevented is astronomical.

The Solution on the Horizon: How Private Health Insurance Bridges the Gap

For those who want to regain control over their healthcare, private medical insurance (PMI) offers a powerful and increasingly popular alternative. At its core, PMI is a policy you pay for that gives you access to private healthcare services, allowing you to bypass NHS queues for eligible conditions.

The single most impactful feature of modern PMI policies in tackling the GP crisis is the Virtual GP service.

This service, now included as a standard benefit with almost every major UK health insurance plan, is a game-changer. It provides policyholders with on-demand access to a qualified, practising GP via a smartphone app or telephone, 24 hours a day, 7 days a week.

Let's compare the experience.

Table 2: Comparing NHS GP Access with a Typical Private Virtual GP Service

| Feature | Standard NHS GP | Private Virtual GP (via PMI) |

|---|---|---|

| Booking Method | Phone call "scramble" at 8am; online forms with delayed responses. | Simple booking via a dedicated smartphone app or phone line. |

| Typical Wait Time | Hours to over 4 weeks for a routine appointment. | Same-day appointments are standard, often available within hours. |

| Availability | Typically Monday-Friday, 8am-6pm. Limited out-of-hours service. | 24 hours a day, 7 days a week, 365 days a year. |

| Appointment Length | Average 9-10 minutes, often feeling rushed. | Typically longer, 15-20 minutes, allowing for a more thorough discussion. |

| Location | Requires travel to a physical surgery, plus waiting room time. | From the comfort of your home, office, or even while on holiday in the UK. |

| Prescription Service | Prescription sent to a local pharmacy for collection. | Private prescription can be sent directly to your home or a nearby pharmacy. |

The benefits are immediate and obvious:

- Unrivalled Speed: The anxiety of waiting disappears. A health concern that arises in the morning can be discussed with a doctor by the afternoon.

- Incredible Convenience: No need to take time off work, arrange childcare, or travel. It fits your life, not the other way around.

- Reduced Burden: You no longer feel like you are "bothering" a busy system. The service is there for you to use as needed.

A virtual GP can handle a huge range of primary care needs: they can offer medical advice, diagnose common conditions, and issue private prescriptions. But their most powerful function within a PMI policy is what they do next.

Beyond the GP: The Full Spectrum of Private Healthcare Access

A private virtual GP is your new front door to healthcare. But private health insurance gives you the keys to the entire house. If the virtual GP believes you need to see a specialist, they don't just add you to a long NHS waiting list. They issue an open referral.

This is where the true power of PMI is unlocked.

- Swift Specialist Referrals: An open referral is your passport to the private sector. You can use it to book a consultation with a specialist consultant – a cardiologist, dermatologist, gynaecologist, or orthopaedic surgeon – often within days or weeks, not the months or even years it can take on the NHS.

- Rapid Diagnostic Tests: The specialist will likely need diagnostic tests to understand your condition. PMI provides fast-track access to crucial scans like MRI, CT, and PET scans, as well as X-rays, ultrasounds, and blood tests. This rapid diagnosis is the cornerstone of effective treatment, ending the "watch and wait" anxiety that plagues so many.

- Choice and Control: In the private sector, you are in the driver's seat. Your insurance policy gives you the power to:

- Choose your specialist consultant from a list of approved experts.

- Choose your hospital from your insurer's extensive network of high-quality private hospitals.

- Choose your appointment and treatment times to fit around your work and life commitments.

- Comprehensive Mental Health Support: Recognising the growing mental health crisis, most insurers now offer significant mental health benefits. This can range from a set number of therapy sessions (e.g., CBT) accessible without a GP referral, right through to full cover for specialist consultations and in-patient psychiatric care, depending on your policy.

This seamless, integrated journey – from a virtual GP call on Monday to a specialist consultation the following week and an MRI scan shortly after – is the core promise of private health insurance. It replaces waiting and worrying with action and answers.

A Critical Caveat: Understanding Pre-Existing and Chronic Conditions

This is the most important section of this guide. It is absolutely crucial to understand what private medical insurance is for, and what it is not for.

Standard private medical insurance in the UK is designed to cover new, acute conditions that arise after your policy begins.

It does NOT cover:

- Chronic Conditions: These are long-term illnesses that cannot be cured, only managed. Examples include diabetes, asthma, hypertension, Crohn's disease, and most types of arthritis. The ongoing management of these conditions will always remain with the NHS.

- Pre-Existing Conditions: This refers to any disease, illness, or injury for which you have experienced symptoms, received medication, advice, or treatment in the years before you took out your policy (typically the last 5 years).

PMI is not a replacement for the NHS. It is a complementary service that works alongside it. The NHS will always be there for emergencies (like a heart attack or a serious accident), for managing your chronic conditions, and for dealing with any health issues you had before you were insured.

PMI is your solution for the new and unexpected acute problems. An acute condition is a condition that comes on suddenly and is likely to respond quickly to treatment, leading to a full recovery. Think of things like:

- A hernia requiring surgery.

- Gallstones needing removal.

- Joint pain that requires a knee or hip replacement.

- Diagnosing and treating a new heart condition.

- Cancer treatment.

When you apply for a policy, the insurer will use a process called "underwriting" to exclude these pre-existing conditions. The two main types are:

- Moratorium Underwriting: The most common type. It's a simple process where the insurer automatically excludes any condition you've had in the last 5 years. However, if you go for a continuous 2-year period after your policy starts without any symptoms, treatment, or advice for that condition, the insurer may reinstate cover for it.

- Full Medical Underwriting (FMU): This requires you to complete a detailed health questionnaire. The insurer then assesses your medical history and lists specific, permanent exclusions on your policy documents. It provides more certainty upfront but can be more complex.

Understanding this distinction is key to having the right expectations and using your policy effectively.

What Does a Private Health Insurance Policy Actually Cover?

Private health insurance is not a one-size-fits-all product. Policies are modular, allowing you to build a plan that suits your needs and budget. It typically starts with a core foundation, to which you can add optional extras.

Table 3: Typical PMI Policy Structure

| Level of Cover | What it Typically Includes | Why it's Important |

|---|---|---|

| Core Cover | In-patient & day-patient treatment (hospital beds, surgery, anaesthetist fees). Comprehensive cancer cover (chemo, radiotherapy, biological therapies). Some basic mental health support. | This is the essential safety net. It covers the cost of major procedures and treatments if you are admitted to hospital, which are often the most expensive bills. |

| Out-patient Cover (Optional Add-on) | Specialist consultations, diagnostic tests, and scans (MRI, CT). Post-operative physiotherapy. | This is the key to fast diagnosis. Without this, you would still need an NHS referral for a specialist, involving a long wait. This add-on is vital to unlock the speed of PMI. |

| Therapies Cover (Optional Add-on) | Physiotherapy, osteopathy, chiropractic, and sometimes podiatry or acupuncture. | Crucial for musculoskeletal issues, sports injuries, and recovery from surgery. Allows you to get hands-on treatment quickly to manage pain and restore mobility. |

| Mental Health Cover (Optional Add-on) | Enhanced cover for therapies like CBT, counselling, and access to psychiatrists and psychologists. | Provides extensive support beyond the basic cover, offering a lifeline for those needing structured mental health treatment without the long NHS waits for services like CAMHS or IAPT. |

Navigating the Market: How to Choose the Right Policy

The UK health insurance market is served by a number of excellent providers, including Bupa, AXA Health, Aviva, and Vitality. While this choice is positive, it can also be complex. Comparing policies, understanding jargon like "excess" and "hospital lists," and deciding on the right level of cover can be overwhelming.

This is where an independent, expert health insurance broker is invaluable. At WeCovr, we specialise in demystifying this process. Our expert advisors compare plans from across the entire market, providing impartial, tailored advice to find a policy that perfectly matches your requirements.

Key factors we help you consider:

- Your Budget: We help you understand the trade-offs between premium cost, your chosen excess (the amount you pay towards a claim), and the level of cover.

- Level of Cover: Do you just want core hospital cover, or is comprehensive out-patient cover for fast diagnosis your priority?

- Hospital List: Insurers offer different tiers of hospitals. A national list provides wide coverage, while a more limited local list can reduce your premium. Premium lists including prime central London hospitals cost more.

- Underwriting: We'll explain the pros and cons of Moratorium vs. Full Medical Underwriting for your specific circumstances.

Navigating these choices can be daunting, which is why using a broker like us at WeCovr is so valuable. We provide impartial advice tailored to your specific needs and budget, ensuring you don't pay for cover you don't need, and that you fully understand the cover you have.

Beyond Insurance: Proactive Health and Added Value

The best modern insurers are no longer just passive payers of claims. They are evolving into holistic health and wellbeing partners, incentivising you to stay healthy. Many policies now come packed with added-value benefits designed to promote a proactive approach to your health, such as:

- Discounted gym memberships.

- Wearable fitness tracker deals.

- Access to online health and wellbeing resources.

- Rewards for healthy behaviour.

- Preventative health screenings.

At WeCovr, we believe in this proactive approach so strongly that we go a step further. In addition to helping you find the perfect policy from the UK's leading insurers, we provide all our customers with complimentary access to CalorieHero, our exclusive AI-powered calorie and nutrition tracking app. It’s our way of supporting your health journey long-term, empowering you to make informed lifestyle choices every day, and adding tangible value beyond the insurance policy itself.

Your Health, Your Choice: Taking Control in 2025

The crisis in GP access is a harsh reality of modern Britain. The days of easily booking a routine appointment and being seen within a few days are, for now, a thing of the past for millions. The consequence of this is not just frustration, but a tangible risk to the nation's health through delayed diagnoses and escalating conditions.

While we all hope for and support a resurgent NHS, you are not powerless in the face of these systemic challenges. Private medical insurance offers a proven, effective, and immediate solution. It empowers you to bypass the queues and take decisive action on your health concerns.

It provides:

- Speed: Access a GP within hours, a specialist within days, and diagnostic tests within a week.

- Choice: You decide the consultant, the hospital, and the time for your treatment.

- Peace of Mind: The immense relief of knowing that should a new health concern arise, you have a plan to deal with it swiftly and effectively.

It is an investment not just in a policy, but in your own health, your family's wellbeing, and your future. In an era of uncertainty, taking control of your healthcare journey is one of the most powerful decisions you can make. Explore your options, speak to an expert, and discover how you can move from waiting and worrying to action and assurance.

Sources

- NHS England: Waiting times and referral-to-treatment statistics.

- Office for National Statistics (ONS): Health, mortality, and workforce data.

- NICE: Clinical guidance and technology appraisals.

- Care Quality Commission (CQC): Provider quality and inspection reports.

- UK Health Security Agency (UKHSA): Public health surveillance reports.

- Association of British Insurers (ABI): Health and protection market publications.