TL;DR

The United Kingdom is facing a silent crisis. It doesn’t arrive with a sudden crash but with a slow, creeping dread—the notification letter from the NHS. It's the confirmation that the pain in your knee, the persistent back ache, or the worrying symptoms you've bravely faced will not be addressed for months, or more likely, years.

Key takeaways

- Speed of Access: This is the primary benefit. Instead of waiting months for a specialist appointment, you can often be seen within days. Instead of waiting over a year for surgery, you can typically have it within a few weeks of diagnosis. This speed is crucial for preventing a condition from worsening and for getting you back to your life and work.

- Choice and Control: With PMI, you are in the driver's seat. You can often choose the specialist or surgeon who treats you, and the hospital where you receive your care. You can schedule appointments and surgery at times that suit you, minimising disruption to your life.

- Enhanced Comfort and Environment: Private hospitals typically offer private en-suite rooms, more flexible visiting hours, and a quieter, more comfortable environment for recovery. This can have a significant positive impact on your mental state and healing process.

- Moratorium Underwriting (Most Common): You don't declare your full medical history upfront. Instead, the insurer applies a blanket exclusion for any condition you've had symptoms, treatment, or advice for in the last 5 years. However, if you then go for a set period (usually 2 years) without any symptoms, treatment, or advice for that condition after your policy starts, the insurer may agree to cover it in the future.

- Full Medical Underwriting (FMU): You provide your complete medical history when you apply. The insurer then assesses it and tells you exactly what is and isn't covered from day one. This provides certainty but means any pre-existing conditions are likely permanently excluded.

UK Health Wait Shock

The United Kingdom is facing a silent crisis. It doesn’t arrive with a sudden crash but with a slow, creeping dread—the notification letter from the NHS. It's the confirmation that the pain in your knee, the persistent back ache, or the worrying symptoms you've bravely faced will not be addressed for months, or more likely, years.

New projections for 2025 paint a stark and deeply concerning picture. The combination of a post-pandemic backlog, systemic workforce pressures, and an ageing population has created a perfect storm. The NHS, a service we rightly cherish, is stretched to its absolute limit. The result? A referral-to-treatment (RTT) waiting list that is not just a statistic, but a source of profound personal and financial turmoil for millions.

For the working-age population, the consequences are particularly devastating. Projections indicate that over a third of working Britons will find their lives upended by these delays. This isn't merely an inconvenience; it's a direct threat to your livelihood, your long-term health, and your financial stability. The pain you endure while waiting isn't just physical—it's the financial strain of being unable to work, the anxiety of a career stalling, and the fear that by the time you're treated, the damage could be irreversible.

This article unpacks the true, multi-faceted cost of waiting and reveals how Private Medical Insurance (PMI) has evolved from a 'nice-to-have' luxury into an essential tool for safeguarding your future.

The Anatomy of a Crisis: Unpacking the 2025 NHS Waiting List Projections

To understand the solution, we must first grasp the sheer scale of the problem. The official figures are sobering, and the 2025 projections, based on current trends from sources like [NHS England](https://www.england.nhs.As of early 2025, the waiting list for elective treatment in England is forecast to hover stubbornly around 7.8 million cases. However, this headline figure masks a more terrifying reality: the number of individuals waiting over a year for treatment. While efforts are made to reduce the longest waits, hundreds of thousands of people remain trapped in a painful limbo, their lives on hold.

The number of people economically inactive due to long-term sickness has surged to a record high of over 2.ons.gov.uk/employmentandlabourmarket/peoplenotinwork/economicinactivity). This isn't a coincidence; it's a direct consequence of a healthcare system unable to provide timely care. People are simply too unwell to work, and the wait for treatment is a key driver.

Where are the longest waits?

While the crisis is system-wide, certain specialities are under immense pressure. These are often the procedures that directly impact a person's ability to work and live a pain-free life.

- Orthopaedics: This includes hip and knee replacements, and spinal surgery. Wait times can routinely exceed 18 months, forcing individuals to live with chronic pain and severely limited mobility.

- Ophthalmology: Procedures like cataract surgery, which can restore sight and independence, face significant backlogs.

- Cardiology: Waiting for diagnostics or treatment for heart conditions is not just stressful; it's clinically dangerous.

- Gynaecology & Urology: Conditions in these areas can cause debilitating pain and have a profound impact on quality of life.

- General Surgery: Hernia repairs and gallbladder removals are considered "routine," yet patients can wait over a year for these life-disrupting operations.

The table below illustrates the stark reality of the waiting list's evolution.

| Year | Official NHS Waiting List (England) | Individuals Waiting Over 52 Weeks |

|---|---|---|

| Feb 2020 (Pre-Pandemic) | 4.4 million | 1,613 |

| Feb 2023 | 7.2 million | 362,000+ |

| 2025 (Projection) | 7.8 million+ | 400,000+ |

Source: NHS England data and forward-looking analysis based on current trends.

This isn't just a queue; it's a roadblock to recovery, and for a growing number of people, it's a direct path to financial hardship.

The £4.2 Million Lifetime Burden: How Health Delays Erode Your Finances & Career

The £4.2 million figure in our headline may seem shocking, but it represents the potential lifetime financial impact on a high-earning individual in their mid-40s whose career is derailed by a long-term health issue exacerbated by treatment delays. While this is an extreme scenario, the underlying mechanics affect millions on a smaller but still life-altering scale.

The financial burden is a three-pronged assault on your security.

1. Direct Loss of Earnings

When you're in too much pain to work, or your mobility is compromised, your income is the first casualty. For many, Statutory Sick Pay (SSP) is the only safety net, providing a mere £116.75 per week (2024/25 rate). This is a fraction of the average UK salary and is wholly insufficient to cover mortgages, bills, and living costs. (illustrative estimate)

Consider a self-employed tradesperson with a bad back waiting 18 months for spinal surgery, or an office worker with severe arthritis in their hands unable to type. The loss of income is immediate and catastrophic. Long-term sickness is a leading cause of debt and financial crisis in the UK.

2. Career Stagnation and Derailment

The hidden, long-term cost is often the most damaging. While you are waiting, your career is not.

- Missed Opportunities: You can't take on that big project or apply for a promotion when you're on long-term sick leave or struggling with daily pain.

- Forced Career Change: Many are forced to leave physically demanding jobs or reduce their hours, permanently lowering their earning potential.

- Early Retirement: A significant number of people in their 50s and 60s leave the workforce entirely due to ill health, decimating their pension pots and long-term financial plans.

This "career scarring" has a compounding effect over a lifetime, impacting everything from pension contributions to your ability to support your family.

3. Escalating Out-of-Pocket Expenses

The irony of the waiting list crisis is that it forces many to go private anyway, but in a piecemeal and expensive fashion. Desperate for answers or relief, people are paying for:

- Private GP Consultations: To get a faster referral or a second opinion.

- Private Diagnostics (illustrative): A single MRI scan can cost between £400 and £800. A consultation with a specialist can be £250-£350.

- Interim Therapies: Paying for physiotherapy, osteopathy, or pain management clinics to cope while waiting for definitive treatment.

This reactive spending drains savings without providing a complete solution, adding financial stress to physical pain.

Let's illustrate with a realistic example:

Meet David, a 48-year-old Project Manager

David develops severe hip pain. His GP suspects osteoarthritis and refers him to an NHS specialist. The wait for the initial consultation is 9 months. During this time, the pain worsens. He's struggling to commute, his sleep is disrupted, and his work performance suffers. He pays £60 a session for weekly physiotherapy just to cope.

After 9 months, the specialist confirms he needs a total hip replacement. He is placed on the surgical waiting list with an estimated wait of 15 months.

David's Financial Breakdown Over the 2-Year Wait:

| Cost Category | Description | Estimated Financial Impact |

|---|---|---|

| Lost Earnings | Missed performance bonus due to reduced output. | -£5,000 |

| Sick Leave | Used up 6 months of sick pay, then moved to SSP. | -£18,000 (vs. full salary) |

| Out-of-Pocket Costs | Private physio, consultations, pain medication. | -£4,500 |

| Career Impact | Overlooked for a Director-level promotion. | -£15,000/year salary increase |

| Total Immediate Cost | Direct financial loss and spending over 2 years. | -£27,500 |

| Long-Term Cost | The lost promotion alone could cost him £250,000+ over the remainder of his career. |

David's story is a common one. It demonstrates how a single health issue, when met with a long delay, can trigger a devastating financial chain reaction.

The Irreversible Toll: When Waiting Turns into Permanent Health Decline

Perhaps the most frightening aspect of the waiting list crisis is the clinical consequence. For many conditions, time is not neutral. Waiting actively causes harm. A treatable condition can become a chronic, life-limiting one.

- Musculoskeletal Issues: A damaged joint that could be fixed with timely surgery can lead to chronic pain, muscle wastage, and altered gait, causing secondary problems in other joints like the back or the other knee.

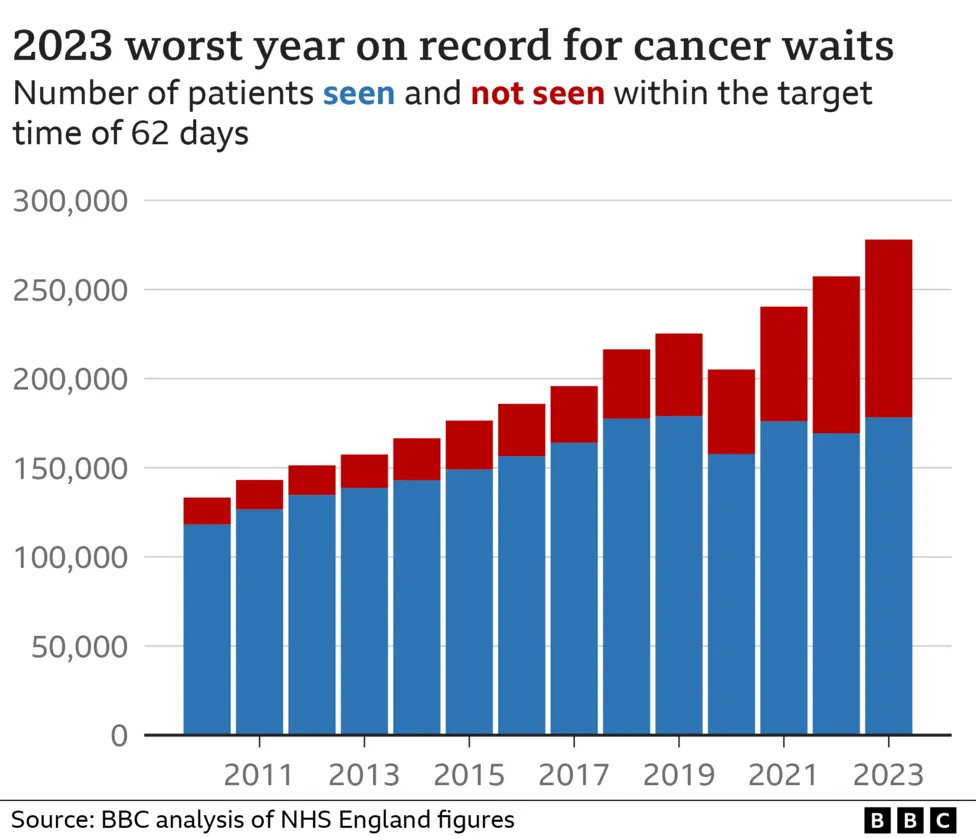

- Cancer: Any delay in diagnosing and treating cancer can allow it to progress to a more advanced stage, drastically reducing the chances of a successful outcome. The "early diagnosis is key" message is undermined by diagnostic bottlenecks.

- Cardiac Conditions: Waiting for treatment for conditions like angina or arrhythmias can increase the risk of a major cardiac event like a heart attack or stroke.

- Mental Health: Living with chronic pain, uncertainty, and financial stress is a recipe for mental health decline. Anxiety and depression are common fellow travellers for those on long-term waiting lists, creating a vicious cycle of poor physical and mental wellbeing.

A condition that is defined as acute—meaning it is curable with treatment—can morph into a chronic one if left untreated for too long. This is a critical distinction that has profound implications for your future health and your ability to get insurance cover later.

Private Medical Insurance (PMI): Your Fast-Track to Recovery

This is where Private Medical Insurance (PMI) enters the picture, not as an indictment of the NHS, but as a pragmatic and powerful tool to work alongside it. PMI gives you a choice—the choice to bypass the queue and get the treatment you need, when you need it.

In its simplest form, PMI is an insurance policy that pays for the costs of private medical care for acute conditions that arise after you take out the policy.

The Core Benefits of PMI: Speed, Choice, and Comfort

-

Speed of Access: This is the primary benefit. Instead of waiting months for a specialist appointment, you can often be seen within days. Instead of waiting over a year for surgery, you can typically have it within a few weeks of diagnosis. This speed is crucial for preventing a condition from worsening and for getting you back to your life and work.

-

Choice and Control: With PMI, you are in the driver's seat. You can often choose the specialist or surgeon who treats you, and the hospital where you receive your care. You can schedule appointments and surgery at times that suit you, minimising disruption to your life.

-

Enhanced Comfort and Environment: Private hospitals typically offer private en-suite rooms, more flexible visiting hours, and a quieter, more comfortable environment for recovery. This can have a significant positive impact on your mental state and healing process.

The difference in timelines is staggering, as the table below shows.

| Procedure | Typical NHS Wait (Referral to Treatment) | Typical Private Timeline with PMI |

|---|---|---|

| Hip/Knee Replacement | 12 - 18+ months | 4 - 6 weeks |

| Cataract Surgery | 9 - 12 months | 3 - 5 weeks |

| Hernia Repair | 9 - 15 months | 4 - 6 weeks |

| MRI/CT Scan | 6 - 12 weeks | 3 - 7 days |

| Specialist Consultation | 4 - 9 months | 1 - 2 weeks |

Navigating the PMI market can be complex, with dozens of policies and providers. That's where an expert broker like WeCovr comes in. We help you compare policies from all the leading UK insurers, such as Bupa, AXA Health, Aviva, and Vitality, ensuring you find a plan that fits your specific needs and budget. Our expertise is in translating your requirements into the right policy.

Decoding Your Cover: What PMI Does (and Doesn't) Include

It is absolutely vital to understand the fundamental rule of standard UK Private Medical Insurance. This is the single most important concept to grasp before considering a policy.

CRITICAL POINT: Private Medical Insurance is designed to cover new, acute medical conditions that arise after your policy begins. It does not, under any circumstances, cover pre-existing conditions or chronic conditions.

Let's break this down with absolute clarity.

Acute vs. Chronic Conditions

This is the central distinction in health insurance.

- An Acute Condition is a disease, illness, or injury that is likely to respond quickly to treatment and lead to a full recovery. Examples include a broken bone, appendicitis, a hernia, gallstones, or the need for a joint replacement. These are the conditions PMI is built for.

- A Chronic Condition is a disease, illness, or injury that has one or more of the following characteristics: it needs ongoing or long-term monitoring, it requires management with medication or check-ups, it has no known cure, or it is likely to recur. Examples include diabetes, asthma, high blood pressure, Crohn's disease, and most types of arthritis. These are excluded from PMI cover.

If you already have symptoms or a diagnosis for a condition before taking out a policy, that is a pre-existing condition and will also be excluded from cover.

How Insurers Assess Pre-Existing Conditions

Insurers use two main methods to handle pre-existing conditions, known as underwriting:

- Moratorium Underwriting (Most Common): You don't declare your full medical history upfront. Instead, the insurer applies a blanket exclusion for any condition you've had symptoms, treatment, or advice for in the last 5 years. However, if you then go for a set period (usually 2 years) without any symptoms, treatment, or advice for that condition after your policy starts, the insurer may agree to cover it in the future.

- Full Medical Underwriting (FMU): You provide your complete medical history when you apply. The insurer then assesses it and tells you exactly what is and isn't covered from day one. This provides certainty but means any pre-existing conditions are likely permanently excluded.

What's Typically Covered vs. Typically Excluded?

| ✅ Typically Covered | ❌ Typically Excluded |

|---|---|

| Surgery as an in-patient or day-patient | Pre-existing conditions |

| Specialist consultations | Chronic conditions (e.g., Diabetes) |

| Advanced diagnostics (MRI, CT, PET scans) | A&E / Emergency services |

| Cancer treatment (often a core feature) | Normal pregnancy and childbirth |

| Out-patient therapies (e.g., physiotherapy) | Cosmetic surgery |

| Mental health support (varies by policy) | Organ transplants |

| Private hospital room and nursing care | Drug and alcohol rehabilitation |

Understanding these boundaries is key to having the right expectations and using your policy effectively.

Tailoring Your Policy: How to Get the Right Cover at the Right Price

One of the biggest misconceptions about PMI is that it's prohibitively expensive. In reality, modern policies are highly flexible, allowing you to tailor the cover to control the cost. Think of it like building a car—you can choose the engine size, the trim level, and the optional extras.

Here are the main levers you can pull to manage your premium:

- The Excess: This is the amount you agree to pay towards a claim. For example, if you have a £250 excess and your treatment costs £5,000, you pay the first £250 and the insurer pays the rest. Choosing a higher excess (£500 or £1,000) can significantly reduce your monthly premium.

- The Hospital List: Insurers have tiered hospital lists. A comprehensive list including prime central London hospitals is the most expensive. Opting for a list that covers high-quality local hospitals but excludes the top London ones can offer substantial savings.

- Level of Out-patient Cover: You can choose a policy that only covers treatment when you're admitted to hospital (in-patient), or you can add cover for out-patient diagnostics and consultations. Many people opt for a limited out-patient cover (e.g., up to £1,000) as a happy medium.

- The "Six-Week Wait" Option: This is a very popular cost-saving feature. With this option, if the NHS can treat you within six weeks for a specific procedure, you will use the NHS. If the NHS wait is longer than six weeks, your private cover kicks in. This effectively protects you from long delays while lowering your premium, as you still rely on the NHS for more promptly available care.

At WeCovr, our specialists can walk you through these options, demystifying the jargon and helping you build a policy that provides robust protection without breaking the bank. Our goal is to find you the most value, not just the cheapest price.

We believe in a holistic approach to wellbeing. That's why, as a WeCovr customer, you also receive complimentary access to our exclusive AI-powered wellness app, CalorieHero. It's our way of going the extra mile, empowering you with tools to proactively manage your diet and health long before you ever need to make a claim.

Is Private Health Insurance Worth It in 2025? A Final Verdict

Faced with the stark reality of 2025's healthcare landscape, the question is no longer "can I afford private health insurance?" but rather, "can I afford not to have it?".

When your ability to earn a living, pursue your career, and live without pain is dictated by a waiting list that stretches for years, the monthly cost of a PMI policy shifts from an expense to an investment. It's an investment in continuity—the continuity of your income, your career progression, and, most importantly, your health.

It provides a guarantee of speed and choice when you are at your most vulnerable. It's the peace of mind of knowing that a diagnosis won't automatically trigger a financial crisis or a permanent decline in your wellbeing. For the working people of Britain, who are the engine of the economy and the bedrock of their families, being sidelined by a treatable health condition is a risk too great to bear.

The NHS will be there for emergencies. It will be there for chronic care. But for the vast and growing chasm of elective treatment, relying on the system as it stands is a gamble. Private Medical Insurance is the bridge across that chasm.

Don't let your health and financial future be decided by a waiting list. Take control today. The expert team at WeCovr is ready to provide you with a free, no-obligation comparison of the UK's top health insurance plans. Safeguard your most valuable assets – your health and your ability to earn.

Sources

- NHS England: Waiting times and referral-to-treatment statistics.

- Office for National Statistics (ONS): Health, mortality, and workforce data.

- NICE: Clinical guidance and technology appraisals.

- Care Quality Commission (CQC): Provider quality and inspection reports.

- UK Health Security Agency (UKHSA): Public health surveillance reports.

- Association of British Insurers (ABI): Health and protection market publications.