TL;DR

The numbers are in, and they paint a sobering picture of healthcare in the United Kingdom. New analysis based on current trends projects that by the end of 2025, a staggering one in five Britons referred for non-emergency hospital treatment will find themselves waiting for over a year. This isn't a statistical anomaly; it's the new reality for millions.

Key takeaways

- Pre-existing Conditions: Any illness or injury you have had symptoms of, received advice for, or been treated for in the years before your policy started (typically the last 5 years).

- Chronic Conditions: Long-term illnesses that cannot be cured, only managed. This includes conditions like diabetes, asthma, hypertension, Crohn's disease, and multiple sclerosis. The day-to-day management of these will always sit with your NHS GP.

- Emergency Care: If you have a heart attack, a stroke, or are in a serious accident, you must call 999 and go to an NHS A&E department. Private hospitals are not equipped for major trauma or emergencies.

- Other Standard Exclusions: These typically include routine pregnancy and childbirth, cosmetic surgery (unless medically necessary following an accident), organ transplants, and self-inflicted injuries.

- Adjust Your Excess: Choosing an excess of £250 or £500 can reduce your monthly premium by 15-30%.

UK NHS Wait Shock

The numbers are in, and they paint a sobering picture of healthcare in the United Kingdom. New analysis based on current trends projects that by the end of 2025, a staggering one in five Britons referred for non-emergency hospital treatment will find themselves waiting for over a year. This isn't a statistical anomaly; it's the new reality for millions.

For decades, the NHS has been the bedrock of our nation's health. Yet, unprecedented pressure has stretched its resources to a critical point. The once-unthinkable year-long wait is fast becoming a grim standard for common procedures like hip replacements, cataract surgery, and hernia repairs.

But the impact of these delays extends far beyond the hospital doors. It creates a ripple effect of "hidden costs" that touch every aspect of our lives – from our physical and mental wellbeing to our financial stability and the nation's economic productivity.

This definitive guide will unpack the data behind the 2025 NHS wait shock. We will explore the profound and often overlooked consequences of waiting for care and, most importantly, detail a powerful and accessible solution: Private Medical Insurance (PMI). Discover how taking control of your healthcare can not only guarantee rapid access to life-saving treatment but also protect your health, your wealth, and your peace of mind.

The 2026 NHS Waiting List Crisis: A Reality Check

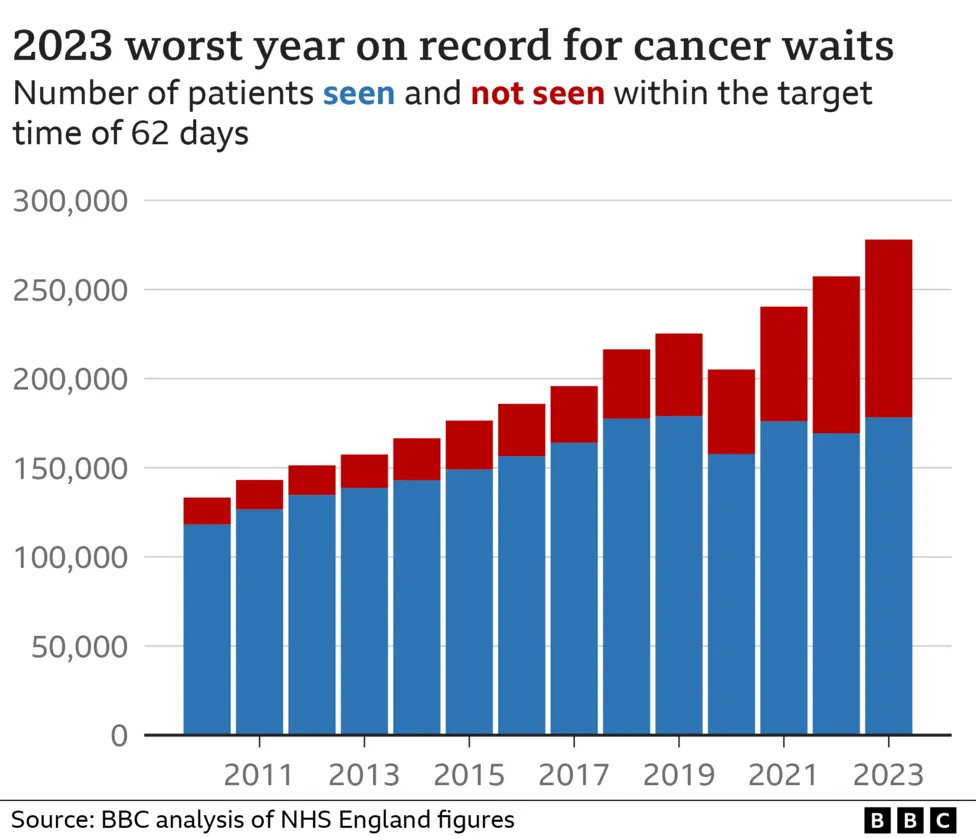

The term 'crisis' is often overused, but a forensic look at the data shows it is entirely appropriate. The official NHS England waiting list for elective treatment, which stood at 4.4 million before the pandemic, is now projected to surge past **8.While the total number is alarming, the most concerning statistic is the growth in long-term waits.

- Pre-Pandemic (Feb 2020): Just 1,613 people were waiting over 52 weeks for treatment.

- Mid-2024: This figure had exploded to over 300,000.

- 2025 Projection: Based on current referral rates and treatment capacity, forecasts indicate that well over 1.5 million people could be waiting over a year for their procedure. This represents a significant portion of the total list.

This isn't just about statistics; it's about people. It's the grandfather who can no longer play with his grandchildren because of a painful knee. It's the self-employed worker losing their business because they can't get the surgery they need to return to work.

A Growing Divide: The Waiting List 'Iceberg'

The official figures, as stark as they are, only tell part of the story. Experts at The King's Fund and other health think tanks refer to the "hidden waiting list" – millions of people who need care but have not yet been officially referred by their GP, often due to difficulties in securing an initial appointment. This means the true demand for NHS treatment is far greater than what is officially recorded.

| Time Period | Official NHS Waiting List (England) | Patients Waiting Over 52 Weeks |

|---|---|---|

| February 2020 | 4.4 million | 1,613 |

| May 2024 | 7.6 million | 302,000 |

| Projected Q1 2025 | 8.5 million+ | 1.5 million+ |

Source: NHS England data and projections based on IFS and Nuffield Trust modelling.

This data illustrates a system under duress, where the promise of timely care is becoming increasingly difficult to fulfil. The consequences of this systemic delay are profound and deeply personal.

More Than a Number: The Hidden Costs of Waiting

Waiting for medical treatment is not a passive activity. For hundreds of thousands of people across the UK, it is an active state of deteriorating health, mounting anxiety, and financial hardship. The true cost isn't measured in hospital budgets, but in quality of life lost.

The Toll on Your Physical & Mental Health

When you're on a waiting list, your condition doesn't simply press pause.

- Physical Deterioration: A treatable joint problem can worsen, leading to muscle wastage, reduced mobility, and the potential need for a more complex operation. Conditions that cause pain often lead to a reliance on painkillers, which can have their own side effects.

- Mental Health Decline: Living with chronic pain and uncertainty is a significant psychological burden. A 2024 study in The Lancet directly linked long healthcare waits to increased rates of anxiety, depression, and feelings of hopelessness. The stress of being unable to work, plan for the future, or live a normal life takes a heavy toll.

- Risk of Complications: For some, the wait can turn an urgent issue into an emergency. A planned hernia repair delayed can become a life-threatening strangulated hernia requiring emergency surgery.

Case Study: David, 58, a retired police officer. David was told he needed a hip replacement and was placed on the NHS waiting list with an estimated 14-month delay. During this time, the pain forced him to give up his hobbies of walking and gardening. He became increasingly isolated, his mobility declined sharply, and the constant pain led to sleepless nights and a diagnosis of clinical depression. His straightforward procedure had spawned a host of secondary health problems.

The Toll on Your Wealth & the UK Economy

The health crisis is inextricably linked to a financial one. The Office for National Statistics (ONS) has consistently reported record numbers of people economically inactive due to long-term sickness – now exceeding 2.8 million people in the UK. Many of these individuals are on NHS waiting lists.

- Loss of Earnings: Being unable to work while waiting for treatment means a direct loss of income, pushing families into financial precarity. For the self-employed, it can mean the end of their business.

- Productivity Drain: For employers, staff on long-term sick leave creates a significant drain on productivity. A 2025 report from the Confederation of British Industry (CBI) estimated that health-related absenteeism and presenteeism (working while ill) costs the UK economy over £100 billion per year.

- The Carer's Burden: The impact extends to family members who may need to reduce their working hours or leave their jobs entirely to provide care, further straining household finances.

The table below illustrates the cascading financial impact of a typical one-year wait for surgery.

| Factor | Direct & Indirect Financial Costs |

|---|---|

| Loss of Income | Potential for 12 months on Statutory Sick Pay (£116.75/week) or zero income for self-employed. |

| Career Impact | Risk of redundancy, missed promotions, loss of professional skills. |

| State Costs | Increased reliance on welfare benefits, reduced tax revenue. |

| Business Costs | Cost of covering absent employee, loss of productivity and institutional knowledge. |

| Personal Spending | Increased spending on private physiotherapy, painkillers, and mobility aids to manage the condition. |

Waiting is not free. It costs our health, our savings, and our economic stability. It's a price that millions are now being forced to pay.

The Proactive Solution: Understanding Private Medical Insurance (PMI)

Faced with this daunting reality, a growing number of people are refusing to be passive participants in a system at its breaking point. They are choosing to take control by investing in Private Medical Insurance (PMI), a powerful tool that provides a direct route to prompt, high-quality medical care.

So, what exactly is PMI?

In simple terms, PMI is an insurance policy that covers the cost of private medical treatment for acute conditions. It is not a replacement for the National Health Service. You will still rely on the NHS for emergency services (A&E), GP appointments, and the management of long-term chronic illnesses.

Think of PMI as a healthcare safety net. It runs parallel to the NHS, offering you a choice. When you are diagnosed with a new, eligible condition, PMI gives you the option to bypass the NHS queue and be treated quickly in a private hospital.

The journey typically works like this:

- You visit your NHS GP for a diagnosis and an open referral. While some insurers now offer a digital GP service, a referral from your own GP is the most common starting point.

- You contact your PMI provider, who will confirm your cover and provide a list of approved specialists and hospitals.

- You book your consultation and subsequent treatment at a time and place that suits you.

- The insurer settles the bills directly with the hospital and specialists.

At WeCovr, we find that our clients' primary motivation is the desire for certainty and speed. They want the peace of mind that comes from knowing that if they or a family member falls ill, they won't be left waiting in pain and anxiety.

The Crucial Caveat: What PMI Does Not Cover

To make an informed decision, it is absolutely essential to understand the limitations of Private Medical Insurance. PMI is a specific product for a specific need, and being clear on its scope is key to avoiding disappointment.

The Golden Rule: PMI is for new, treatable (acute) conditions that arise after your policy begins.

An acute condition is a disease, illness, or injury that is likely to respond quickly to treatment and lead to a full recovery (e.g., a hernia, cataracts, joint problems, most cancers).

Standard PMI policies will NOT cover:

- Pre-existing Conditions: Any illness or injury you have had symptoms of, received advice for, or been treated for in the years before your policy started (typically the last 5 years).

- Chronic Conditions: Long-term illnesses that cannot be cured, only managed. This includes conditions like diabetes, asthma, hypertension, Crohn's disease, and multiple sclerosis. The day-to-day management of these will always sit with your NHS GP.

- Emergency Care: If you have a heart attack, a stroke, or are in a serious accident, you must call 999 and go to an NHS A&E department. Private hospitals are not equipped for major trauma or emergencies.

- Other Standard Exclusions: These typically include routine pregnancy and childbirth, cosmetic surgery (unless medically necessary following an accident), organ transplants, and self-inflicted injuries.

Understanding these exclusions is not a drawback; it's a fundamental part of how PMI is designed to be affordable and effective. It focuses resources on providing world-class care for unexpected, acute health problems, complementing the essential services provided by the NHS.

The Tangible Benefits: How PMI Puts You in Control

The core value of private medical insurance can be distilled into two words: speed and choice. When facing a health concern, these two factors can transform your experience, your outcome, and your outlook.

Here are the tangible benefits you can expect:

1. Rapid Access to Specialists and Diagnosis

This is the number one reason people buy PMI. Instead of waiting months for an initial consultation with an NHS specialist, you can typically be seen within days or weeks. This speed is crucial for peace of mind and for getting a definitive diagnosis and treatment plan in place swiftly.

2. Choice of Consultant and Hospital

PMI empowers you. You are not simply assigned to the next available surgeon. You can research and choose a leading specialist for your specific condition from your insurer's approved list. You can also select a hospital that is convenient for you, known for its expertise, or offers a more comfortable environment.

3. A Comfortable and Private Environment

Recovering from surgery or illness is easier in a calm and private setting. A key benefit of private treatment is access to a private, en-suite room with amenities like a TV, choice of food, and more flexible visiting hours. This can significantly improve your recuperation experience.

4. Access to Advanced Treatments and Drugs

The private sector is often faster to adopt new technologies, surgical techniques, and groundbreaking drugs. Some treatments and medications may be available privately long before they are approved by the National Institute for Health and Care Excellence (NICE) for widespread NHS use. For conditions like cancer, this can be life-changing.

5. Comprehensive Cancer Care

This is a cornerstone of most PMI policies. Cover typically extends far beyond surgery, including full access to chemotherapy, radiotherapy, specialist consultations, and often experimental treatments and biological therapies. Many policies also provide support like home nursing and palliative care.

6. Integrated Mental Health Support

Modern PMI policies recognise the deep link between physical and mental health. Most now offer significant cover for mental health treatment, providing access to psychiatrists, psychologists, and therapists without the long waits often found in the NHS system.

To see the difference in practice, consider a typical patient journey for a knee replacement.

| Stage | NHS Pathway | Private Pathway with PMI |

|---|---|---|

| GP Referral | Referral to NHS Orthopaedics. | Open referral to a specialist. |

| Specialist Wait | 3-6 months (average). | 1-2 weeks. |

| Diagnostic Scans | Wait of 4-8 weeks for MRI. | Scans often done same/next day. |

| Wait for Surgery | 9-18 months. | 2-4 weeks after consultation. |

| Choice | Assigned surgeon and hospital. | Choice of leading surgeon and hospital. |

| Hospital Stay | Ward with 4-6 beds. | Private, en-suite room. |

| Post-Op Physio | Group sessions, limited number. | One-to-one sessions, often more included. |

| Total Time | 12 - 26 months | 4 - 8 weeks |

The difference is not just one of time; it's one of control, comfort, and confidence in your care.

Demystifying the Cost: What Can You Expect to Pay for PMI in 2026?

A common misconception is that private medical insurance is an unaffordable luxury reserved for the very wealthy. In reality, modern policies are highly flexible, allowing you to tailor your cover to suit your budget.

For a healthy, non-smoking 35-year-old, a mid-range policy can start from as little as £45 per month. For a 50-year-old, this might rise to around £80-£100 per month. While premiums increase with age and the level of cover chosen, the cost is often comparable to a premium gym membership or a daily coffee habit. When weighed against the cost of lost earnings and diminished health from a long wait, many see it as an essential investment.

Several key factors determine the cost of your premium.

| Factor | Impact on Premium | Explanation |

|---|---|---|

| Age | High | The single biggest factor. Risk of illness increases with age. |

| Level of Cover | High | Comprehensive plans with full out-patient cover cost more than treatment-only plans. |

| Excess | Medium | A higher voluntary excess (the amount you pay per claim) will significantly lower your premium. |

| Hospital List | Medium | Choosing a list that excludes expensive central London hospitals can reduce costs. |

| Location | Medium | Premiums are often higher in major cities where private hospital costs are greater. |

| Smoker Status | Low-Medium | Smokers are considered higher risk and will pay more than non-smokers. |

How to Manage Your Premiums

You have significant control over the cost of your policy. Here are the main levers you can pull:

- Adjust Your Excess: Choosing an excess of £250 or £500 can reduce your monthly premium by 15-30%.

- The '6-Week Wait' Option: This is a popular way to cut costs. Your policy will only kick in if the NHS waiting list for your required treatment is longer than six weeks. If the NHS can treat you within that timeframe, you use the NHS. If not, your private cover is activated.

- Tailor Your Hospital List: Opting for a list of quality local hospitals rather than a comprehensive national list that includes the most expensive facilities can offer substantial savings.

- Review Out-patient Cover: You can choose a policy with full out-patient cover, a limited amount (e.g., £1,000), or no out-patient cover at all, which would mean you pay for initial consultations and scans yourself but are covered for the expensive surgical procedure.

Choosing Your Shield: How to Select the Right PMI Policy

With a wide range of insurers and policy options, choosing the right PMI can feel overwhelming. Understanding the key components is the first step to finding a plan that protects you effectively.

Underwriting: The Policy's Foundation

This is how the insurer assesses your medical history and decides what they will and won't cover.

- Moratorium (Mori) Underwriting: This is the most common and straightforward option. You don't need to declare your full medical history upfront. The insurer automatically excludes any condition you've had symptoms, treatment, or advice for in the 5 years before the policy starts. However, if you then go for a set period (usually 2 years) without any trouble from that condition, the insurer may reinstate cover for it.

- Full Medical Underwriting (FMU): This requires you to complete a detailed health questionnaire. The insurer will review your medical history and state explicitly from the outset what is excluded from your policy. It provides more certainty but can be more complex to set up.

Key Policy Options to Consider

- Out-patient Limits (illustrative): Decide if you want full cover for specialist consultations and diagnostic tests, or if you're happy with a capped amount (e.g., £1,000) or none at all.

- Cancer Cover: This is a critical area. Check the level of cover. Does it include advanced therapies, palliative care, and follow-up consultations? Most policies offer enhanced cancer cover as standard or as an add-on.

- Mental Health Cover: If this is a priority, look for policies that offer comprehensive support for both in-patient and out-patient psychiatric treatment.

- Therapies: Check the limits for services like physiotherapy, osteopathy, and chiropractic care, which are vital for recovery.

Navigating these options and the small print of each provider's offering is where expert guidance is indispensable. This is where an independent broker like WeCovr becomes invaluable. We are not tied to any single insurer. Our role is to understand your specific needs, concerns, and budget. We then compare plans from all major UK insurers—including Bupa, AXA Health, Aviva, and Vitality—to find a policy that provides the right protection for you.

Furthermore, as part of our commitment to our clients' long-term wellbeing, we provide complimentary access to our AI-powered nutrition app, CalorieHero. It's a small way we go above and beyond, helping you stay on top of your health goals long before you ever need to make a claim.

PMI and the NHS: A Partnership, Not a Rivalry

It is vital to see private medical insurance not as an abandonment of the NHS, but as a complementary partner to it. A robust private healthcare sector can, in fact, alleviate some of the pressure on the NHS.

Every person who chooses to use PMI for an eligible procedure frees up a space on an NHS waiting list for someone else. You remain an NHS patient, fully entitled to its services. You will still see your NHS GP, and you will absolutely rely on the NHS for any emergency care.

Having PMI simply gives you an additional resource. It's about creating a personal safety net that ensures when you need planned care, you can access it on your own terms, without delay.

Is Private Medical Insurance Worth It in 2026?

As we face the reality of 2025's healthcare landscape, the question "Is PMI worth it?" takes on a new urgency.

The answer lies in a simple value judgement. What price do you put on your health? What is the value of your ability to work, to be free from pain, to live your life without the shadow of a year-long wait for care?

The cost of not having a safety net is no longer abstract. It can be measured in:

- Months or years of pain and discomfort.

- Thousands of pounds in lost earnings.

- The deterioration of a treatable condition into a chronic problem.

- The profound emotional and psychological strain on you and your family.

When a monthly premium—often less than the cost of a family mobile phone plan—can eliminate these risks, the value proposition becomes clear. It is a pragmatic investment in your single most important asset: your health and wellbeing.

The NHS remains one of our country's greatest achievements. But in an era of unprecedented demand, relying solely on a system under immense strain is a gamble many are no longer willing to take. Private Medical Insurance offers a path to certainty, speed, and control. It is the definitive tool for navigating the challenges of 2025 and guaranteeing that when you need it most, you will receive the best possible care, right away.

Sources

- NHS England: Waiting times and referral-to-treatment statistics.

- Office for National Statistics (ONS): Health, mortality, and workforce data.

- NICE: Clinical guidance and technology appraisals.

- Care Quality Commission (CQC): Provider quality and inspection reports.

- UK Health Security Agency (UKHSA): Public health surveillance reports.

- Association of British Insurers (ABI): Health and protection market publications.