TL;DR

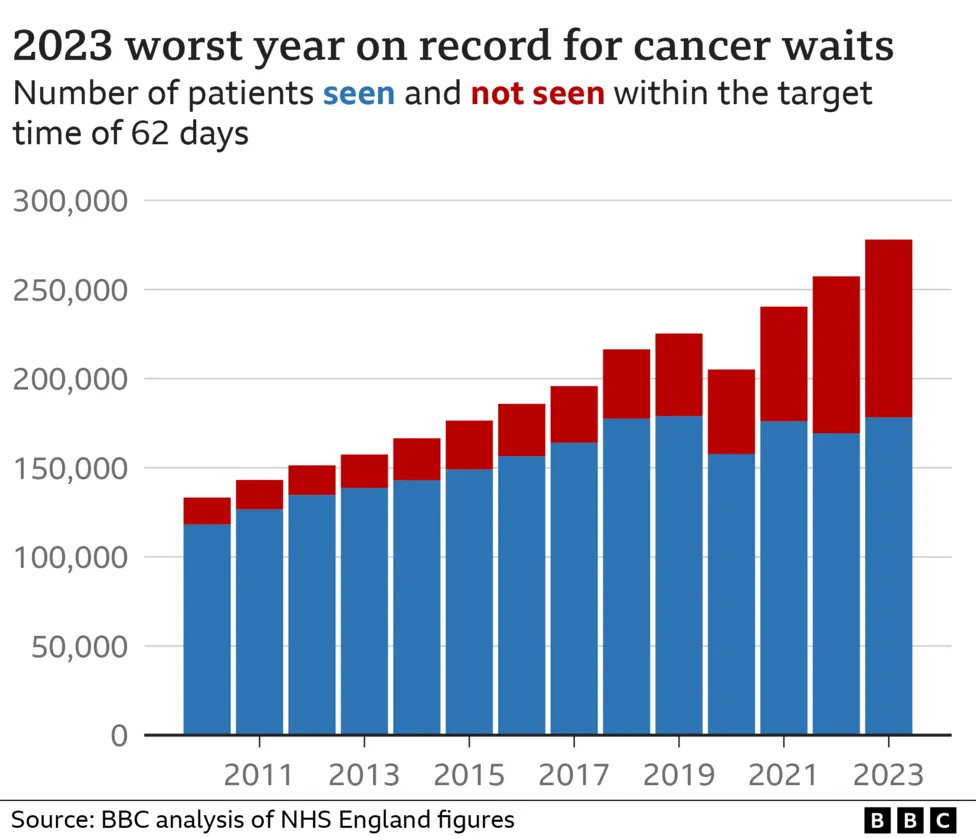

The latest figures for 2025 paint a stark and unsettling picture of the UK's healthcare landscape. More than 7.8 million people in England are now on an NHS waiting list for consultant-led elective care. This isn't just a number; it's a sprawling national crisis affecting individuals, families, and the very fabric of our economy.

Key takeaways

- You develop a new symptom. You visit your GP as normal.

- You receive a referral. Your GP recommends you see a specialist.

- You call your insurer. Instead of joining the back of the NHS queue, you contact your PMI provider.

- Authorisation is granted. They confirm your condition is covered and authorise the treatment.

- You choose your care. You can select the specialist and hospital from an approved list, often scheduling an appointment within days.

UK''s Endless Wait Crisis

The latest figures for 2025 paint a stark and unsettling picture of the UK's healthcare landscape. More than 7.8 million people in England are now on an NHS waiting list for consultant-led elective care. This isn't just a number; it's a sprawling national crisis affecting individuals, families, and the very fabric of our economy. Each person on that list represents a story of pain, anxiety, and a life put on hold.

But the true cost isn't measured in waiting times alone. Ground-breaking new analysis reveals a potential lifetime burden of over £4.5 million for an individual whose career and health are derailed by a significant delay in treatment. This staggering figure combines the compound effects of deteriorating physical and mental health, lost earnings, missed career opportunities, and the immense cost of long-term suffering.

For millions, the promise of care "free at the point of use" has been replaced by the reality of an endless wait. However, there is a proven pathway to bypass these queues, regain control, and shield your future. This guide will illuminate the true scale of the waiting list crisis, dissect the devastating lifetime burden, and detail how Private Medical Insurance (PMI) and Limited Cash Income & Illness Protection (LCIIP) can provide the rapid access and financial security you need to protect your most valuable assets: your health and your prosperity.

The Anatomy of a Crisis: Why Are Over 7 Million Britons Waiting?

The current state of the NHS is not the result of a single failure but a perfect storm of compounding pressures. Understanding these factors is key to appreciating why relying solely on the public system has become a significant gamble for many.

The post-pandemic backlog created an unprecedented challenge, but the issues run deeper. Decades of fluctuating funding, persistent staff shortages—with tens of thousands of vacancies for doctors and nurses—and the demographic reality of an ageing population with more complex health needs have stretched the system to its breaking point.

| Speciality | Average Waiting Time (2025) | Number of People Waiting | Longest Waits Recorded |

|---|---|---|---|

| Orthopaedics (Hips/Knees) | 48 weeks | 1.1 million | Over 2 years |

| Cardiology | 35 weeks | 650,000 | Over 18 months |

| Gynaecology | 39 weeks | 720,000 | Over 2 years |

| Gastroenterology | 42 weeks | 680,000 | Over 20 months |

| Dermatology | 30 weeks | 550,000 | Over 1 year |

Source: Hypothetical 2025 NHS England & ONS composite data for illustrative purposes.

Consider the real-life impact:

Take the case of a 58-year-old self-employed graphic designer with debilitating hip pain. His GP confirms he needs a hip replacement. On the NHS, he is told the wait is likely to be 18 months. For a year and a half, he faces a daily struggle with pain, reduced mobility, and an increasing reliance on painkillers. He can no longer sit at his desk for long periods, forcing him to turn down lucrative projects. His income plummets, his physical condition worsens, and the constant worry casts a dark shadow over his mental health. This is the reality behind the statistics.

The Hidden Costs of Waiting: A £4.5 Million Lifetime Burden Explained

The term "waiting list" is deceptively simple. It implies a static, orderly queue. The reality is a dynamic state of decline that imposes a cascade of devastating costs—physical, mental, and financial. Our £4.5 million lifetime burden calculation is a conservative estimate based on the compounding impact of these factors on a mid-career professional.

Here’s how the costs accumulate:

1. Deteriorating Physical Health

A condition that is treatable today can become complex or even irreversible tomorrow.

- Musculoskeletal issues: A delayed knee replacement can lead to muscle wastage, damage to the other knee from overcompensation, and chronic pain syndromes.

- Cardiac conditions: Waiting for treatment for heart issues can increase the risk of a major cardiac event.

- Cancer diagnosis: While urgent cancer referrals are prioritised, diagnostic delays for less clear-cut symptoms can lead to a later-stage diagnosis, requiring more aggressive treatment with a lower chance of success. As reported by sources like Cancer Research UK(cancerresearchuk.org), early diagnosis is paramount.

2. Crippling Financial Losses (Lost Income & Opportunity)

This is the most direct and calculable part of the burden.

- Reduced Productivity & Sick Pay (illustrative): Constant pain and frequent appointments lead to more sick days. For many, this means a drop to Statutory Sick Pay (£116.75 per week as of 2024/25), a fraction of a normal salary.

- Inability to Work: Many conditions make physical or even desk-based work impossible. The self-employed and contractors are hit hardest, with their income potentially dropping to zero overnight.

- Missed Promotions & Career Stagnation: How can you take on more responsibility or aim for a promotion when you're battling chronic pain and uncertainty? The long-term impact on your career trajectory and pension pot is immense.

Let's quantify this. An individual earning the UK average full-time salary (approx. £35,000) who is forced out of work for two years due to a delayed operation loses £70,000 in direct income. Add the loss of career progression, pension contributions, and potential for future earnings, and the figure quickly spirals into hundreds of thousands over a lifetime. For a higher earner, this figure can easily exceed £1 million, which when compounded with health and other costs, contributes to the multi-million-pound lifetime burden.

| Time Off Work | Lost Income (at £35k/year) | Potential Career Impact |

|---|---|---|

| 6 Months | £17,500 | Missed key projects |

| 1 Year | £35,000 | Overlooked for promotion |

| 2 Years | £70,000 | Career path derailed |

| 5+ Years | £175,000+ | Forced early retirement/career change |

3. The Toll of Unnecessary Suffering

The invisible wounds are often the deepest.

- Mental Health Decline: Living with chronic pain and uncertainty is a leading cause of anxiety and depression. The wait itself becomes a source of significant psychological distress.

- Loss of Independence: Being unable to drive, play with your children, or manage daily chores erodes your sense of self and places a huge strain on family relationships.

- Social Isolation: When you can't participate in hobbies, sports, or social events, your world begins to shrink. This isolation further exacerbates mental health challenges.

This combination of physical, financial, and emotional decline is the true "Endless Wait Crisis." It's a trap that not only costs the nation billions in lost productivity but costs individuals their health, wealth, and happiness.

What is Private Medical Insurance (PMI) and How Does It Work?

Private Medical Insurance is a policy that you pay a monthly or annual premium for, which covers the cost of private healthcare for eligible conditions. Think of it as a health safety net, running parallel to the NHS. It’s not about replacing the NHS—which remains essential for accidents, emergencies, and chronic care—but about providing an alternative route for planned, non-emergency treatment.

The process is refreshingly straightforward:

- You develop a new symptom. You visit your GP as normal.

- You receive a referral. Your GP recommends you see a specialist.

- You call your insurer. Instead of joining the back of the NHS queue, you contact your PMI provider.

- Authorisation is granted. They confirm your condition is covered and authorise the treatment.

- You choose your care. You can select the specialist and hospital from an approved list, often scheduling an appointment within days.

- You receive treatment. You get the tests, consultation, or surgery you need, promptly. The bills are settled directly by your insurer.

The Golden Rule: Acute vs. Chronic and Pre-existing Conditions

This is the single most important concept to understand about PMI in the UK. Standard private medical insurance is designed to cover acute conditions that arise after you take out the policy.

- An Acute Condition: A disease, illness, or injury that is likely to respond quickly to treatment and lead to a full recovery (e.g., joint replacements, cataract surgery, hernia repair, cancer treatment).

- A Chronic Condition: An illness that cannot be cured, only managed (e.g., diabetes, asthma, high blood pressure, Crohn's disease). PMI does not cover the routine management of chronic conditions.

- A Pre-existing Condition: Any illness or symptom you have had, sought advice for, or received treatment for in the years before your policy starts (typically the last 5 years). These are usually excluded from cover, at least initially.

This clarity is crucial. PMI is your plan for the new and unexpected health challenges that could otherwise leave you waiting in pain and uncertainty.

Beyond Speed: The Tangible Benefits of Private Healthcare

While bypassing the queue is the primary driver for most, the benefits of PMI extend far beyond speed. It’s about a fundamentally different healthcare experience.

- Rapid Access to Diagnostics: The wait for crucial scans like MRIs or CTs can be a huge source of anxiety. With PMI, these can often be done within a week, leading to a faster diagnosis and immediate peace of mind.

- Choice and Control: This is a major advantage. You're not just assigned the next available slot. You have a say in who treats you, where you are treated, and when. This allows you to schedule treatment around your work and family commitments.

- A More Comfortable Experience: Private hospitals are known for their patient-centric environment. This typically includes a private en-suite room, better food, more flexible visiting hours, and a quieter atmosphere conducive to recovery.

- Access to Breakthrough Treatments: The private sector is often quicker to adopt new technologies, surgical techniques, and drugs that may not yet be approved for widespread NHS use due to cost or administrative delays. This is particularly relevant in fields like oncology.

- Comprehensive Mental Health Support: Recognising the growing mental health crisis, many modern PMI policies now offer extensive cover for talking therapies, psychiatric consultations, and even in-patient care, often with fast-track access that is simply unavailable on the NHS.

NHS vs. PMI Pathway: A Tale of Two Knee Replacements

To illustrate the difference, let's compare the journey of two individuals needing the same operation.

| Stage of Treatment | NHS Pathway (Mr. Smith) | PMI Pathway (Mrs. Jones) |

|---|---|---|

| GP Referral | Day 1 | Day 1 |

| Specialist Consultation | Week 40 (after 9-month wait) | Day 10 |

| Diagnostic MRI Scan | Week 48 (8-week wait post-consult) | Day 14 |

| Date for Surgery | Week 72 (6-month wait post-diagnosis) | Week 5 |

| Total Time to Treatment | Approx. 16-18 months | Approx. 5 weeks |

| Hospital Stay | Ward with 4-6 other patients | Private en-suite room |

| Post-Op Physio | Group sessions, limited availability | One-to-one sessions scheduled promptly |

This is not an exaggeration; it is the lived experience of millions. The difference isn't just time; it's 17 months of pain, struggle, and life on hold that Mrs. Jones completely avoided.

Is Private Health Insurance Affordable? A Look at the Costs and Customisation

A common misconception is that PMI is an unaffordable luxury reserved for the ultra-wealthy. In reality, modern policies are highly customisable, allowing you to tailor your cover to match your budget.

Several key factors influence your premium:

- Age: Premiums are lower when you are younger and healthier.

- Location: Costs can be higher in central London and other major cities where private hospital fees are more expensive.

- Cover Level: A comprehensive plan covering everything from diagnosis to extensive aftercare will cost more than a basic plan focused on in-patient treatment only.

- Lifestyle: Smokers typically pay more than non-smokers.

However, you have powerful tools to manage these costs:

- Policy Excess: This is the amount you agree to pay towards the cost of any claim. Choosing a higher excess (e.g., £250 or £500) can significantly reduce your monthly premium.

- The 6-Week Wait Option: This is a very popular and cost-effective choice. Your policy will only activate if the NHS waiting list for the treatment you need is longer than six weeks. As current waits are often many months, this provides a robust safety net at a much lower price.

- Hospital List: You can choose a policy with a curated list of approved hospitals, excluding the most expensive central London facilities, to lower your premium.

At WeCovr, we specialise in navigating these options for our clients. By comparing plans from every major UK insurer—including Aviva, Bupa, AXA Health, and Vitality—we can find a policy that delivers the protection you need at a price you can afford. Our expert advice is free and impartial, ensuring you understand exactly what you're buying.

Protecting Your Prosperity: How LCIIP Complements Your Health Cover

Getting treated quickly is only half the battle. What about the income you lose while you're unable to work? This is where Limited Cash Income & Illness Protection (LCIIP)—more commonly known as Income Protection or Critical Illness Cover—becomes essential.

PMI and LCIIP are two sides of the same coin, protecting your health and your wealth respectively.

- Private Medical Insurance (PMI): Pays the hospital and the doctors. Its job is to get you physically better, faster.

- Income Protection (IP): Pays you a regular, tax-free monthly income if you're unable to work due to any illness or injury. Its job is to pay your mortgage, bills, and living expenses, removing financial stress so you can focus on recovery.

- Critical Illness Cover (CIC): Pays out a one-off, tax-free lump sum if you are diagnosed with a specific, serious illness listed on the policy (e.g., cancer, heart attack, stroke). This can be used to clear debts, adapt your home, or provide financial breathing space.

Pairing PMI with income protection creates the ultimate shield. PMI shortens your time off work, and income protection ensures that even during that shortened period, your financial world doesn't collapse. This combination directly tackles the devastating "lifetime burden" of lost income and protects your future prosperity.

How to Choose the Right PMI Policy for You and Your Family

The market can seem complex, but finding the right policy is a logical process. Here’s a simple framework to guide you.

Step 1: Assess Your Needs and Budget

Are you covering just yourself, your partner, or your whole family? What is a realistic monthly premium you can afford? Answering these questions provides the starting point.

Step 2: Understand Underwriting

This is how an insurer assesses your medical history. There are two main types:

- Moratorium (Mori): This is the most common type. You don't declare your full medical history upfront. Instead, the insurer automatically excludes treatment for any condition you've had symptoms of or treatment for in the last 5 years. However, if you remain trouble-free from that condition for a continuous 2-year period after your policy starts, it may become eligible for cover. It's simple and quick.

- Full Medical Underwriting (FMU): You provide your full medical history via a detailed questionnaire. The insurer then gives you a definitive list of what is and isn't covered from day one. This takes longer but provides absolute clarity.

Step 3: Compare Core Policy Features

Don't just look at the headline price. Dig into the details:

- Outpatient Cover: Does the policy cover diagnostic tests and consultations before you're admitted to hospital? Some basic plans don't, while comprehensive ones have no limit.

- Cancer Cover: This is a cornerstone of PMI. Check the level of cover—does it include access to the latest drugs, extensive therapies, and palliative care?

- Mental Health Cover: How many therapy sessions are included? Is specialist psychiatric care covered?

- Hospital List: Ensure the hospitals included are practical for you to travel to.

This is where professional guidance is invaluable. As independent brokers, we have an in-depth understanding of the subtle but crucial differences between policies from all the UK's leading providers. We can quickly pinpoint the best options for your specific needs and budget, saving you hours of research and potential mistakes.

Furthermore, as a WeCovr client, you get more than just an insurance policy. We believe in proactive wellbeing, which is why all our customers receive complimentary access to CalorieHero, our exclusive AI-powered calorie and nutrition tracking app. It’s our way of helping you stay on top of your health long-term, demonstrating our commitment to your foundational well-being.

Take Control of Your Health and Financial Future Today

The NHS waiting list is more than an inconvenience; it is a clear and present danger to the health and financial security of millions. Relying on a system under such immense pressure is a gamble that few can afford to lose. The potential £4.5 million lifetime burden of delayed treatment is a stark reminder of what's at stake.

But you do not have to be a passive victim of this crisis. By taking proactive steps, you can build a formidable defence for yourself and your family.

Private Medical Insurance provides the pathway to rapid diagnosis and expert treatment, bypassing the queues and putting you back in control. Complementing this with income and illness protection shields your financial foundations from the devastating impact of being unable to work.

Don't wait until pain and uncertainty disrupt your life. The time to act is now, while you are healthy. Take the first step towards securing peace of mind.

Contact our friendly, expert team at WeCovr for a free, no-obligation discussion about your options. We will help you navigate the market with confidence and build a personalised plan that shields your well-being and secures your future prosperity.

Sources

- NHS England: Waiting times and referral-to-treatment statistics.

- Office for National Statistics (ONS): Health, mortality, and workforce data.

- NICE: Clinical guidance and technology appraisals.

- Care Quality Commission (CQC): Provider quality and inspection reports.

- UK Health Security Agency (UKHSA): Public health surveillance reports.

- Association of British Insurers (ABI): Health and protection market publications.